Mega 2Q23 Credit Report – It’s simple: No new financing? No new loans (Part I)

Operadora Mega usually takes a few days until it releases its management discussion and analysis (MD&A) and holds its earnings call, but given the levels at which the company’s bond is trading, we didn’t want to wait for those before giving our initial takeaways from the 2Q23 results submitted to Mexican stock exchange BIVA. (We will publish Part II of our analysis following the earnings call).

The non-bank financial institution (NBFI) has claimed for several quarters to be on the hunt for new financing to fund its loan origination. While the decision to keep its loan portfolio steady in 2023 came as a relief (See our 4Q22 Credit Report), the company still needs to raise new funding to meet that goal.

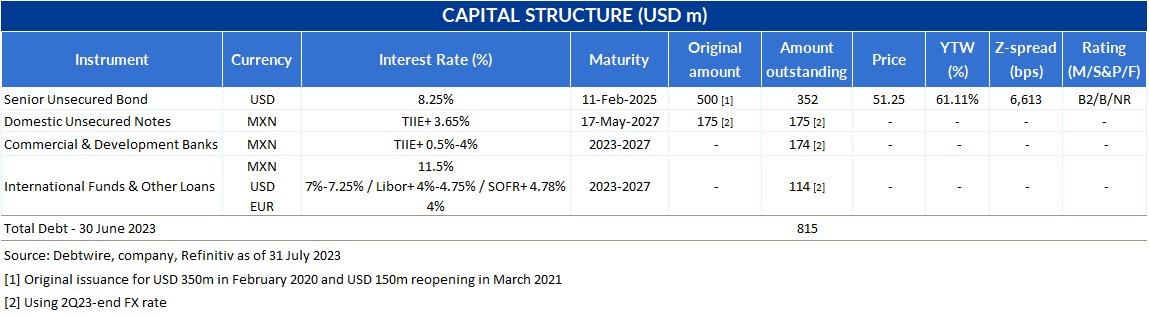

Still, Mega hasn’t announced any new deals for a while now. The lack of new financings can also be seen in the debt breakdown included in the BIVA report (apart from the fact that the amounts in MXN of the USD-denominated liabilities have reduced thanks to the appreciation of the Mexican currency).

As such, after suffering a small reduction in 1Q23, the loan portfolio shrunk even further in 2Q23 (See Figure 1). The reason is simple – in the absence of fresh funds, Mega needs to use the cash generated from the loan collections (interest and principal) to service its debt and cover operating costs.

Mega only provides the exact number of the quarterly loan origination at the MD&A (while comments on loan collections usually arise during the earnings call), but the BIVA results also shed light on the reduction in the concession of new lending by Mega. As we have commented in previous reports, clients of the leasing business (the company’s largest segment) put upfront 20% of the market value of the asset that is subject to the lease agreement. The company records those deposits as a liability (the so-called “Sundry creditors for cash collateral received”), and the accounting entry of the respective deposits disappear from the balance sheet (in a non-cash, accounting-only action) all at once at the end of the lease agreement, when the client exercises a de facto free purchase option on the physical asset.

The balance of the sundry creditors for cash collateral received significantly dropped quarter-over-quarter (QoQ) in 2Q23 (See Figure 2). This can only mean that Mega isn’t originating enough leasing loans to replace the ones that are maturing.

NPL ratio keeps growing, but concern about overall portfolio’s health eases

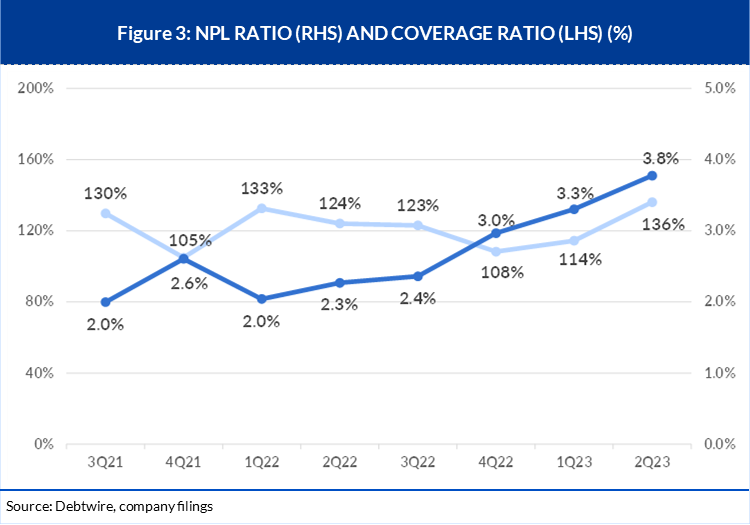

The non-performing loan (NPL) ratio rose for a fifth consecutive quarter, finishing 2Q23 at 3.8%, up from 3.3% three months earlier (See Figure 3). As such, the NPL ratio has increased almost two-fold since the end of 1Q22.

However, beyond this obvious negative trend, there is another angle by which to examine the portfolio’s health, which has eased our concerns somewhat this quarter – the stage 2 segment. As we indicated in the 1Q23 Credit Report, the stage 2 includes loans that have payment delays of more than 30 days but less than 90, and therefore aren’t counted yet as non-performing, despite their deterioration.

We were worried in our previous report about the fact that the size of the stage 2 segment had ballooned compared to the end of 2022, maybe hinting at an overall deterioration of the company’s loan portfolio. Once it is categorized as stage 2, a loan can only evolve in the following ways as time passes by – be transferred to stage 1 (thanks to either a restructuring or to a partial payment that reduces the late payments to no more than 30 days), be fully repaid and thus disappear from the balance sheet, or move to stage 3 if the delays exceed the 90-day threshold and thus it becomes officially non-performing.

Although the breakdown of those movements between stages is only disclosed in the annual reports (so we are only able to see them from December-end to December-end), the BIVA report does include the balance of each of the stages. And we saw a positive change there. While the balance of the stage 3 (i.e. the NPL category) rose MXN 71m, or 12.5%, QoQ to MXN 635m (USD 37m) at the end of 2Q23 from MXN 564m as of 1Q23, the stage 2 reduced by MXN 387m over the same period, to MXN 978m from MXN 1,365m (See Figure 4).

Management told us the previous quarter that three mid-sized clients were struggling with their payments (thus increasing the stage 2 segment), but that the company was in negotiations at least with the largest one to bring it back on track with a payment schedule. Considering the 2Q23 numbers, it seems that those talks may have proved successful. Therefore, while the balance of loans with payment delays of more than 30 days but less than 90 remains well above historical levels, the improvement seen in 2Q23 is clearly a step in the right direction.

A service of

Start your trial. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in