Loan Highlights 9M24: Leveraged loans and refinancing consolidate Americas and EMEA’s comeback

Powered by Debtwire data, Loan Highlights reviews loan market activity across North America, EMEA, and APAC in 9M24. All data correct as of 27 September 2024.

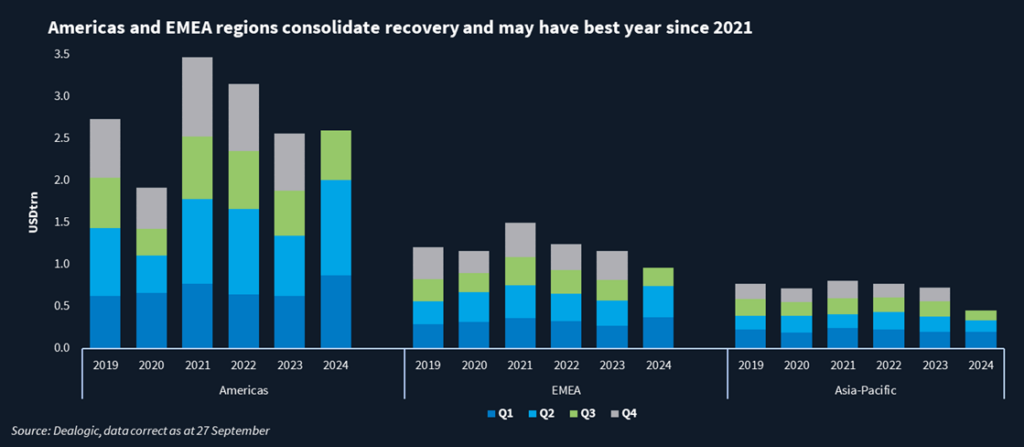

The loan market has responded to interest rate cuts in the main economies around the world and issuance in the Americas, EMEA and Asia-Pacific regions is on the way to having its best year since 2021, Dealogic data shows. The three regions combined have issued USD 4.01trn by the end of 3Q24, 25% over 9M23 (USD 3.194trn) and 5% over 9M22 (USD 3.804trn) figures.

The Americas remains the most prolific region for loans. Beyond historically having the highest overall issuance, it has experienced the most impressive recovery in 2024. The volume issued in nine months (USD 2.6trn) has already overtaken the issuance for the full year 2023 (USD 2.56trn). There’s also a 40% growth year to date, compared to January-September last year (USD 1.8trn). The volume is also 26% higher than the 2019-2023 nine-month average.

Numbers for the EMEA region are also positive. The 9M24 issuance (USD 965bn-equivalent) is 20% higher in the year-over-year comparison and the second-best figure since 2019 – behind only 2021’s USD 1.05bn.

Expectations that central banks were set to cut interest rates in the US and Europe at some point this year had already been energising borrowers in the Americas and EMEA in previous quarters. With the more expansive monetary policy in place, expectations are high for the fourth quarter with issuance in both Americas and EMEA on pace to have their best year since 2021, at least.

The APAC region remains a different story so far this year. Since 2Q24, the volume has been below historical averages. The region has printed USD 453bn in 9M24, 20% down in the YoY comparison and 18% below the 2019-2023 average for nine months (USD 554bn).

Read more in the full report.

To continue reading and get access to more content...

A service of

Start your trial. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in