InterCement Special Credit Report – What would the price of the new bond be?

On 26 June, InterCement’s Argentine subsidiary Loma Negra [BCBA:LOMA] announced a USD 52m-equivalent dividend, of which USD ~25m will go to the parent. The next day, InterCement unveiled an agreement to sell its Mozambique and South Africa operations for an enterprise value of USD 265m (as of 1Q23, net debt was USD 10m, so USD 255m for InterCement). Although these were expected events and part of our base-case view on how the situation would be resolved, many market participants have cast doubt about the execution risk. However, as more steps are completed, this risk decreases and the price of the 2024s will rise, as we saw last week.

The Brazil-based cement company’s financial advisor is now building a model to assess what a “sustainable” capital structure looks like. It can then recommend a maturity schedule for the debentures (domestic bonds) and where would they will reside — at the holding company level or at the Brazilian subsidiary level. It can also determine the characteristics of the new bond to be issued (coupon and tenor) and where an IPO of the Brazilian subsidiary is necessary and how much needs to be raised. This last point is probably intertwined with the size of the debenture and at which level it resides.

In terms of sequence, after the financial advisor’s recommendation, the company will probably first have to negotiate with the debenture holders, and then propose an exchange for the international bondholders. As a result, and following some conversations we had with investors over the last couple of weeks, we decided to try to hypothesize what the alternatives and prices for a new bond would be. The key elements are: (a) coupon rate (plain vanilla or with a PIK option?), (b) tenor (5 or 7 years?), (c) collateral and hence the discount rate (how many shares of Loma Negra?)

Regarding the coupon, management has already mentioned that the coupon of a new bond would be higher than the current 5.75%. We are clearly talking about an overall coupon in the range of 8%-9% (the company will probably not want to have a double-digit coupon). However, an investor told us he has done the math with a portion of the coupon with a PIK option, so we will include this possibility.

The most interesting discussion is the collateral for the new bond, which, in our view, will probably influence the yield at which it trades. The most logical outcome would be for InterCement to give the totality of its Loma Negra shares as collateral. In 2017 when Loma Negra held an IPO, LTM EBITDA was USD 240m, net debt was USD 235m, and given that the market cap reached USD 2.5bn, the implied EV/EBITDA was 11.5x. Today, LTM EBITDA as of 1Q23 was USD 235m, and we estimate the pro-forma net debt after the dividend payments to be USD 260m, for an implied EV/EBITDA of 4.5x.

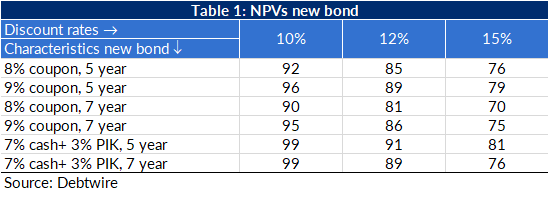

NPV simulation results

From the six scenarios in tables 1 and 2, the first conclusion is that in all cases, prices are significantly above current levels, with the 8% bullet 7-year bond with a discount rate of 15% offering the lowest NPV at a price of 70. On the other side of the spectrum, when we assume 7% cash coupon plus 3% PIK (whether 5-year or 7-year) with 10% discount rates, the price is almost par, which makes sense.

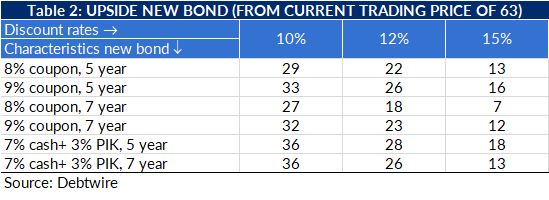

If the discount rate is 15%, then the upside is between 7 and 18 points. At 12% it goes up to between 18 and 28, and if it’s 10%, the upside can be as much as 36 points, which is 57% from current prices.

The discussion, then, is probably about the appropriate discount rate. In part, it will depend on how sustainable the market views InterCement’s capital structure to be (ie IPO yes or no? remaining debenture at holdco, Brazil or split?) and what the collateral is worth. At current prices, InterCement’s stake in Loma Negra is worth USD 420m. Therefore, assuming the outstanding amount of a new bond to be USD 500m, we are talking about a coverage ratio of 84%.

In addition, we expect the price of Loma Negra’s shares to increase if the opposition party wins in Argentina’s presidential elections in October-November (the most likely scenario, in our view). Without taking a view on how much the shares could go up, we do know that if they go up to USD 8.2 per ADR (up 20% from current prices), it would imply an EV/EBITDA multiple of almost 6x, which is not unreasonable, and then the coverage ratio would be 100%. In that scenario, the discount rate can’t be 10% (or lower). In that case, if one believes the company will be able to agree on a reasonable outcome with debenture holders and that the Argentine economy will be better off than it is today, there is a trade to be made here, with the 2024s trading at 63.

A service of

Start your trial. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in