Full Year 2024 European Direct Lender Rankings

European direct lending market rebounded in 2024, propelled by sponsor-led dealmaking

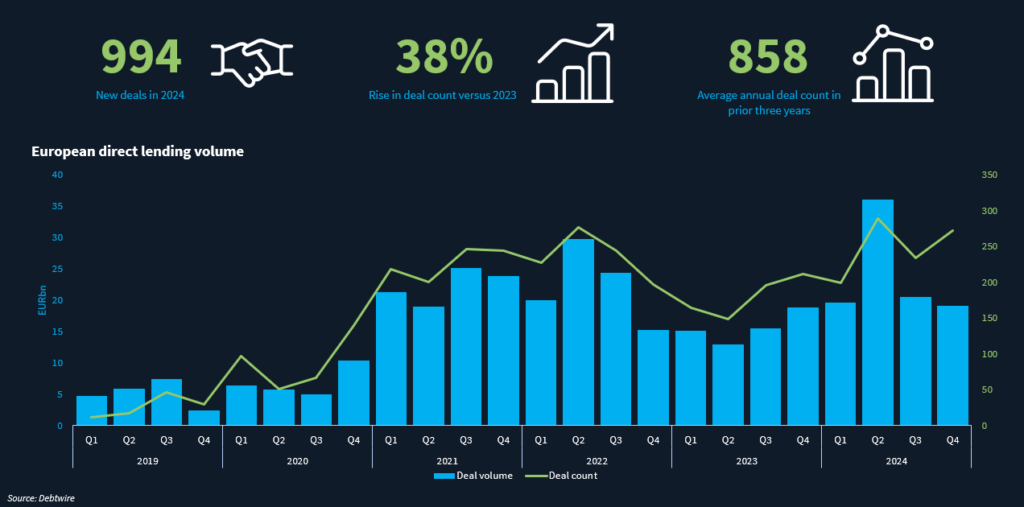

European direct lending accelerated sharply in 2024, with 994 deals completed over the year—a 38% increase from 2023 and well above the prior three-year annual average of 858 transactions, according to Debtwire’s FY24 European Direct Lender Rankings Report. The figures highlight private debt’s continued expansion, as direct lenders played a central role in financing leveraged buyouts and corporate acquisitions, further encroaching on the territory of traditional syndicated loans and high-yield bonds.

The resurgence of financial sponsor-led dealmaking was a key driver of growth. More than one-third of all direct lending proceeds in 2024 were allocated to leveraged buyouts (LBOs), while high-yield bonds and syndicated leveraged loans accounted for less than 10% of new LBO issuance. This shift underscores direct lenders’ growing dominance in private equity platform acquisitions, with sponsors increasingly turning to unitranche and club financings to secure certainty of execution for new-money deals.

In 4Q24, the average margin on direct lending facilities increased to 706bps over the reference rate, up from 645bps in 3Q24, while net leverage declined slightly to 4.7x EBITDA, down from 5.2x in the previous quarter. In comparison, pricing in the syndicated leveraged loan market stood at 405bps in 4Q24, with net leverage at 4.5x. The widening pricing gap reflects direct lenders’ ability to command a premium for flexible structuring and faster execution, particularly in competitive auction processes where private credit continues to outmanoeuvre banks.

From a sectoral perspective, technology was the dominant industry, with over EUR 30bn in direct lending issuance in 2024. Meanwhile, ESG-linked financing activity slowed considerably, reflecting a broader pullback from the highs witnessed in 2022, when EUR 70bn of ESG-linked deals were completed. In 2024, this figure dropped to EUR 27bn, as borrowers and lenders shunned sustainability-linked incentives in a more selective lending environment.

With direct lending activity surging, capital formation remained robust. The largest fundraise of the year came from Ares Management, which raised EUR 33.6bn – including leverage – reinforcing investor confidence in the asset class. As institutional demand for private credit strategies continues to grow, lenders have expanded their capital bases to meet the increasing financing needs of private equity sponsors.

As 2024 drew to a close, direct lenders firmly established themselves as the financing partners of choice for private equity-backed transactions, offering scale, certainty, and bespoke solutions at a time when traditional markets remain constrained, especially when it came to LBO financings.

European Direct Lender Rankings – FY24

Private credit’s expansion in 2024 saw Ares Management maintain its leadership in the European direct lending market, topping Debtwire’s FY24 European Direct Lender Rankings across multiple categories. As direct lenders continued to displace syndicated markets, several firms solidified their foothold across various segments, from large-cap financings to small-cap lending and ESG-linked deals.

Ares Management led the Europe-wide direct lender rankings, completing 37 deals and capturing 5.26% of total market share. Following closely were Goldman Sachs Private Capital, which executed 33 transactions with a 4.69% share, and Blackstone Credit, which rounded out the top three with 32 deals and a 4.55% share.

When factoring in add-on financings, Ares extended its dominance with 84 transactions, representing 7.75% of the market. Eurazeo followed in second place with 55 deals and a 5.07% share, while Goldman Sachs Private Capital secured third with 52 transactions and a 4.80% share.

The rankings for Western Europe closely mirrored broader European trends, with Ares leading at 36 deals and a 5.33% share. Goldman Sachs Private Capital followed with 33 transactions, representing a 4.89% share, while Blackstone Credit placed third with 32 deals and a 4.74% share.

Sustainability-linked financings saw Eurazeo emerge as the leader with 24 ESG-linked deals, capturing 12.12% of the market. Ares followed with 20 transactions and a 10.10% share, while Pemberton completed 18 deals, representing 9.09% of the market.

Goldman Sachs Private Capital dominated the large-cap segment, completing 28 transactions and securing a 17.72% share. Blackstone Credit followed with 21 deals and a 13.29% share, while Apollo Global Management placed third with 20 transactions, representing 12.66% of the market.

In the mid-market segment, Pemberton led with 20 deals and an 8.77% share. Ares and Muzinich shared second place with 18 transactions each, representing 7.89% of the market. Eurazeo and Tikehau followed closely with 14 deals each and a 6.14% share.

CVI topped the small-cap rankings with 14 transactions and a 9.59% share. Fiduciam followed with 12 deals, capturing 8.22% of the market, while HF Private Debt placed third with nine transactions and a 6.16% share.

In junior debt financing, Equita Capital and Park Square tied for first place with five deals each, representing 12.20% of the market. Oquendo Capital followed with four transactions and a 9.76% share. Ares, Blackstone Credit, Eurazeo, Goldman Sachs Private Capital, and MV Credit shared fourth place, each executing three deals and securing a 7.32% share.

Regional Breakdown

In the UK, Ares and Blackstone Credit tied for the lead with 19 deals each, capturing 8.15% of the market. Apollo and Investec Private Debt followed with 18 transactions and a 7.73% share, while Goldman Sachs Private Capital ranked fifth with 15 deals, representing 6.44% of the market.

In France, CIC Private Debt led with 11 deals and an 10.38% share. Eurazeo placed second with 10 transactions and a 9.43% share, while Tikehau followed with nine deals, capturing 8.49% of the market.

In the DACH region (Germany, Austria, Switzerland), HF Private Debt topped the rankings with nine transactions, representing 8.04% of the market. Berenberg Private Capital followed with eight deals and a 7.14% share, while Bright Capital placed third with seven transactions, securing a 6.25% share.

In Benelux, Kartesia led with seven deals and an 8.86% share. Muzinich and Partners Group tied for second place with five transactions each, representing a 6.33% share. Apera and Ares ranked fourth, each executing four deals and capturing a 5.06% share.

In the Nordics, TureInvest claimed the top position with five transactions and a 12.50% share. CVC Credit followed with four deals, representing 10.00% of the market. Arcmont, Cordet Capital, KKR Credit, PSP Invest, and Sixth Street shared third place, each executing three transactions and capturing a 7.50% share.

In Southern and Eastern Europe, CVI led with 15 deals and an 11.19% share. Muzinich followed with 12 transactions and a 8.96% share, while Anthilia placed third with 11 deals, representing 8.21% of the market.

For a deeper dive into sectoral and regional trends, see the full FY24 European Direct Lender Rankings Report.

by Josh O’Neill with analytics from Ben Watson

Debtwire’s direct lender rankings highlight the key players in the private debt market. The report contains active direct lender fund rankings, along with market analysis.

For more Loan League Tables, click here.

For more research, insights and analysis, click here.

A service of

Start your trial. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in