DISH Network serves up disappointing 1Q23 results; liquidity burn could lead to further secured debt issuances or asset sales

by John Sinna

Notes:

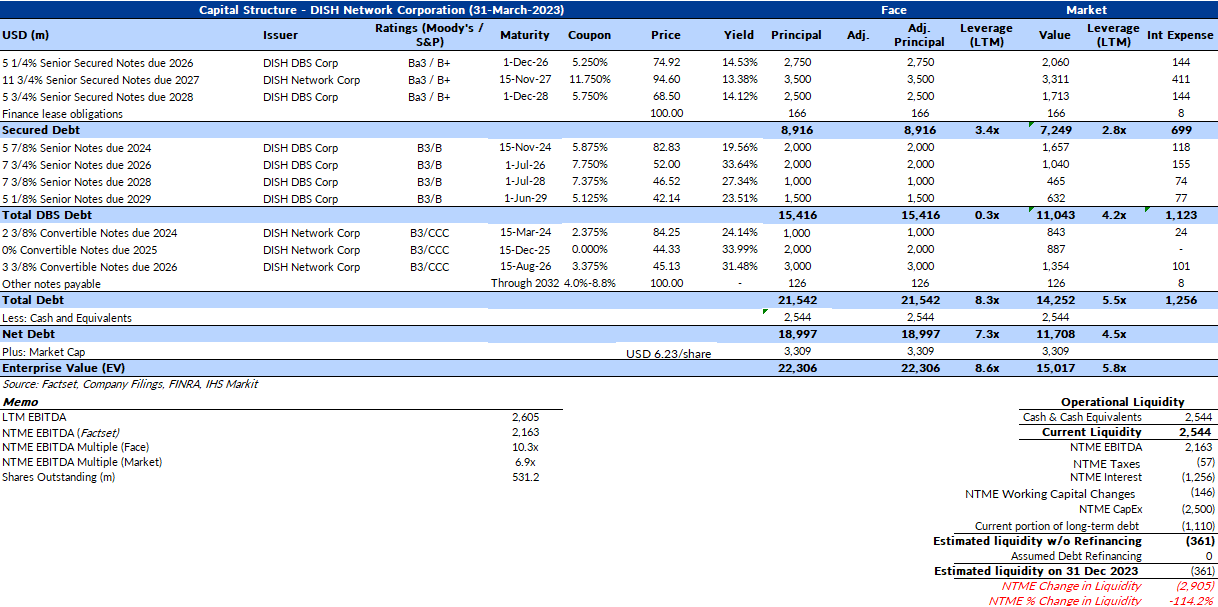

(1) DISH DBS Corp secured bonds due 2026 and 2028 are secured by security interests in substantially all existing and future tangible and intangible assets of DISH DBS and its principal operating subsidiaries on a first priority basis, subject to certain exceptions. Net proceeds from the notes were used to make an intercompany loan to DISH Network pursuant to a Loan and Security Agreement Dated 26 November 2021. Any collateral pledged as security the holders of the notes are subordinated in right of payment to Dish DBS’ senior unsecured notes.

(2) Dish Network secured bonds due 2027 are secured on a first priority basis by security interests, in favor of the secured parties, in the collateral, which consists primarily of interests in wireless spectrum licenses within the 600 MHz band (“the Spectrum Collateral”) owned by one of the secured guarantors and any additional subsidiaries of ours that may be added as guarantors from time to time and equity interests in the Spectrum Collateral guarantor(s) and DISH DBS Corp.

Overview

DISH Network Corporation [NASDAQ: DISH] is a connectivity company that provides television entertainment and technology with its satellite DISH TV and streaming SLING TV services. In 2020, the company became a nationwide wireless carrier through the acquisitions of Boost Mobile and Ting Mobile. It is currently building a nationwide 5G wireless network.

Recent Events

In October 2022, DISH was rumored to have explored a deal with DISH CEO Charlie Ergen’s SPAC in order to fund the remaining build-out of its 5G network. The rumored deal would have Boost Mobile merge with Conx Corp. (“Conx”), and as part of the merger, move financial responsibility for the completion of the Boost Mobile 5G network build-out to Conx and away from DISH. Ergen suggested DISH needs up to USD 10bn in additional funding to complete the Company’s 5G rollout. Boost Mobile’s founder Peter Adderton reportedly partnered with at least one private equity sponsor to explore a bid for the Boost Mobile business to prevent this merger.

On 7 Nov 2022, DISH completed a secured debt offering of USD 2.0bn 5-year non-call 2.5 year paper with an 11.75% coupon that was priced at 98.171 to yield 12.25%. Proceeds from the offering were earmarked for general corporate purposes as well as the continued buildout of the 5G network.

On 7 Dec 2022, DISH launched the beta version of its Boost Infinite mobile plan with a USD 25-a-month lifetime price guarantee. A nationwide rollout was expected during 1Q23.

On 17 Jan 2023, DISH priced an additional USD 1.5bn of its 2027 secured notes at 102, up from an initial expectation of USD 500m. Proceeds from the offering were earmarked for general corporate purposes as well as the continued buildout of the 5G network, and to refinance the 5% Senior Notes due March 2023.

On 13 March 2023, DISH lost a patent dispute case in Utah and the plaintiff, ClearPlay, was awarded USD 469m in damages. The case has been ongoing since 2014 and is likely to go appeal.

On 4 May 2023, DISH settled a patent dispute with Peloton Interactive, Inc (“PTON”). As part of this settlement, PTON agreed to pay DISH USD 75m. The net amount received by DISH and timing of this payment remain unknown.

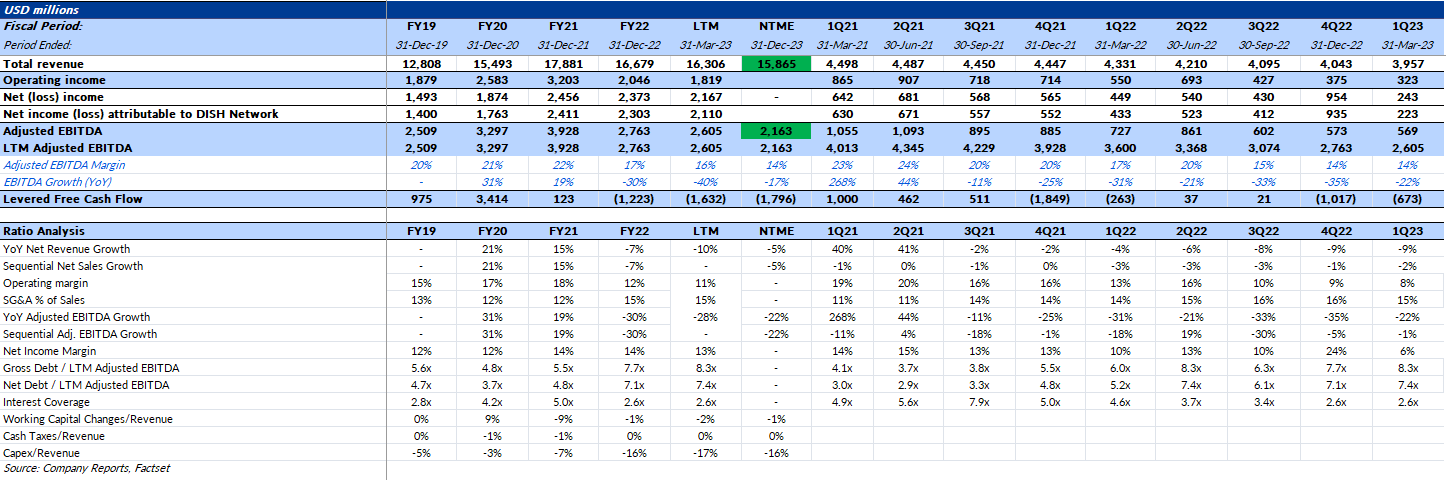

On 8 May 2023, DISH released 1Q23 earnings with 1Q23 revenue of USD 3.96bn missing estimates of USD 4.06bn. Pay-TV subscribers of 9.20m came in below expectations for 9.34m and Sling TV subscribers of 2.10m also missed estimates for 2.20m. Wireless subscribers exceeded estimates, printing 7.91m for 1Q23 versus estimates for 7.68m.

Financials

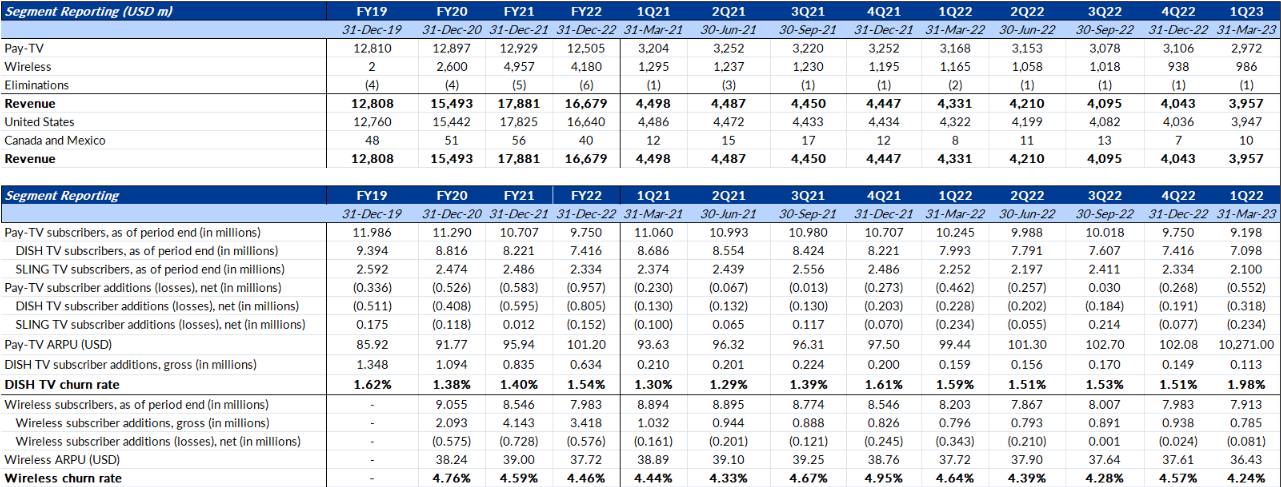

DISH reported revenue of USD 3.96bn for 1Q23, versus USD 4.33bn for 1Q22, driven by higher subscriber churn rate, especially in the DISH TV business. The company had 9.20m pay-TV subscribers as of quarter end, down 552,000 QoQ and 1.05m YoY, due to accelerated cord-cutting, shifting consumer behavior, increased competition, and one-time issues relating to the 1Q23 cyber-security issue. Management suggested some customers were not able to connect with customer service in a timely manner and subsequently canceled service. DISH had 7.91m retail wireless subscribers, down 81,000 QoQ and 290,000 YoY, mainly due to the shutdown of T-Mobile’s CDMA Network and ongoing competitive pressures. DISH is scrambling to hit the key 70% US population coverage level in order to have the option to offer better devices and services to customers, most specifically iPhone devices for the post-paid business.

The operating margin for 1Q23 was 8%, versus 13% in 1Q22, due to increased cost of sales and SG&A as a percentage of sales. This is the crux of the DISH situation – DISH’s growth aspirations, namely in wireless, are swimming against the tide as customer counts recede and the estimated costs to complete its 5G network continue to increase. The Company can no longer milk the cash cow that was the television service business to finance the wireless business.

Adj. EBITDA for 1Q23 was USD 569m, down from USD 727m in 1Q22 due to declines in revenue over the same period slightly offset by lower operating costs. Levered free cash flow was negative USD 673m for 1Q23 versus negative USD 263m for 1Q22, driven by changes in working capital and increased YoY capital expenditures.

For FY23, Factset estimates a decline in revenue to USD 15.87bn or -5% versus FY22 and a decline in Adj. EBITDA to USD 2.16bn. On the 1Q23 call, management suggested FY23 capex will come in below FY22, with most of the spend front-end loaded ahead of the June 2023 milestone (70% coverage). No specific guidance was provided and the FY23 estimate for USD 2.5bn assumes a slight decline YoY. DISH then expects to have a pause on more meaningful network growth capex until sometime in FY24 or FY25.

Management continues to remain somewhat cryptic about its 800mHz option with T-Mobile. The network is already built out and ready to go, and worth “billions” of US dollars, based on DISH’s view of replacement cost. Using a probability weighted valuation methodology, DISH believes this asset is worth USD 5.3bn. The issue for DISH is financing. Management did disclose on the 1Q23 call that the option had recently been extended for at least 60 days and that if DISH ultimately doesn’t exercise, it faces a USD 72m payable (penalty) to T-Mobile. Should the FCC approve the extension, the exercise deadline will move to 1 July, 2023.

Valuation

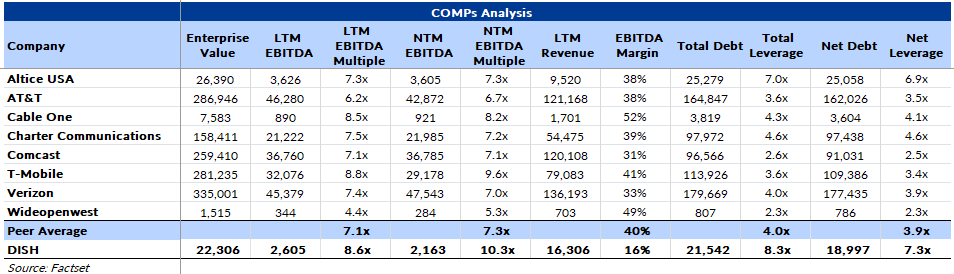

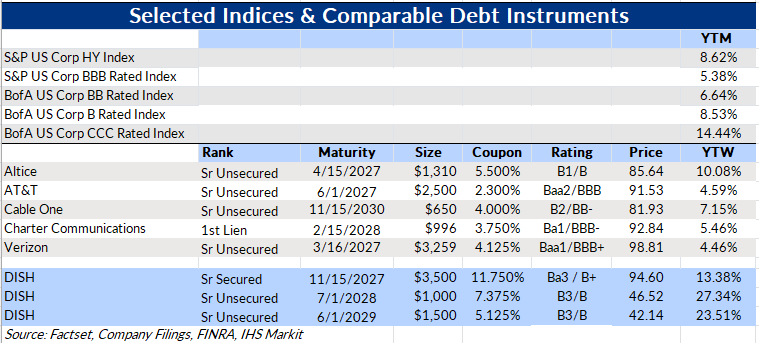

DISH is currently trading at an LTM EV/EBITDA multiple of 8.6x versus a peer average of 7.1x. The NTME EV/EBITDA multiple is 10.3x versus a peer average of 7.3x. Total leverage is 8.3x compared with a peer average of 4.0x, and net leverage is 7.3x versus a 3.9x average for its peers. DISH’s secured debt appears to be fully covered based on current estimates and offers yields that are meaningfully wide to the indices. Investors need to remain mindful of the likelihood that DISH will issue more secured debt in FY2023 in order to address ongoing capex requirements for the 5G network project, address future unsecured debt maturities starting in early 2024, and fill the expected looming general liquidity shortfall.

DISH’s 2024 unsecured paper trades at a premium to the longer dated maturities as well as valuation expectations based on the relatively higher potential for full refinancing / retirement at par with proceeds from new debt issuance. The longer dated unsecured paper trades relatively in line with current valuation expectations and wide to the indices as DISH will need to issue more secured debt in the near term, thereby further subordinating unsecured paper as financial performance remains dicey, and the potential for other events, such as distressed exchange offers or a more formal restructuring activity could be part of the future playbook if new debt financing is not a viable option. Based on current estimates, we and our colleagues at Xtract Research believe DISH has capacity to issue approximately USD 3.5bn in additional secured debt at the DISH DBS Corp. level, which appears to be the path of least resistance, all else being equal.

On the Q4/FY2022 earnings call, management suggested they have the flexibility to refinance the March 2024 convertible notes with an equity component. On the more recent 1Q23 call, management suggested this refinancing might be “equity like”, hinting at the desire to refinance with another convertible offering, which seems like a challenging endeavor given the trading price of the equity and potential dilution from equitizing the debt at par. We believe DISH will use this capacity, including looking to exchange the 2024 unsecured paper for new secured paper in order to address near term liquidity and maturity challenges.

While this additional capacity provides DISH with short-term runway, absent improved financial performance and/or more accommodating market conditions, DISH will find it challenging to manage maturities after 2024, which is reflected in the relative price of its post 2024 obligations. Management also mentioned on the 1Q23 call that the debt markets are “not really open to us” since its existing debt is trading at very rich YTMs, and that DISH is “asset rich”. Clearly management is also looking at monetizations, and perhaps specifically the 800mHz option, as sources of liquidity if needed.

Notes:

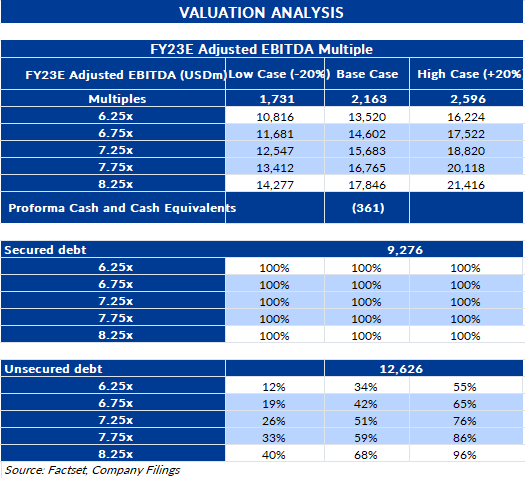

(1) Assumes DISH plugs the USD 361m liquidity gap with additional secured financing.

A service of

Start your trial. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in