DebtDynamics EMEA | Last frontier: Common currency conquers non-Eurozone countries to dominate lev loan market

Since its creation, the euro has been the most relevant currency in the European leveraged loan market. The most obvious choice for companies based in countries such as Germany and France has had a substantial comparative advantage, which can easily explain its preponderance.

Nevertheless, euro-denominated syndicated loans have expanded their dominance in recent years, leaving little to no room for other currencies in the European leveraged market.

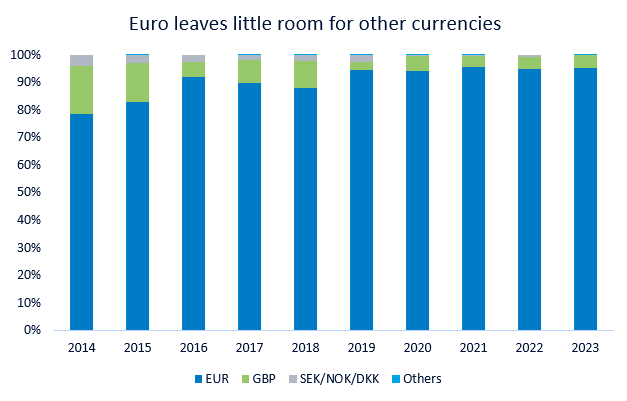

According to Debtwire data, the share of the European leveraged loan syndication market denominated in the EU common currency jumped from 80% in 2015 to levels closer to 95% since 2019.

Source: Debtwire

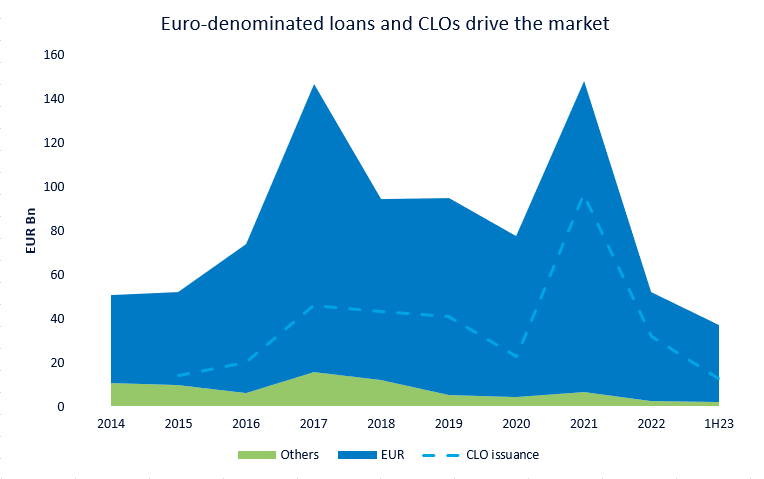

The growth in the EU’s official currency dominance happened in parallel with the expansion of the European CLO market, which is predominantly based on euro-denominated loans. It has meant that European issuers seeking to issue loans in currencies other than the euro face limited demand and risk alienating an essential group of investors.

On the other hand, the CLO managers have created significant demand and an incentive to issue in euros. The amount analysis shows that the volume issued in non-euro currencies has fluctuated from EUR 4.5bn-equivalent and EUR 15.6bn-equivalent between 2014 and 2021, indicating a smaller but continuous market for this paper. The non-euro issuance share was squeezed by the impressive growth the euro-denominated market experienced during the timespan. Then, in the past year and a half, when the interest rates rose, issuance fell across different currencies.

Source: Debtwire / Creditflux

Little room for local currencies

An analysis of the two main non-eurozone regions in Western Europe, the Nordic countries and the UK, shows clearly where and when the euro-denominated paper has gained decisive room.

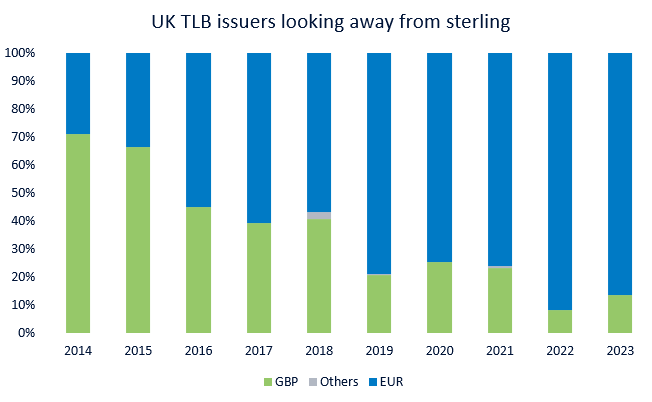

In the pre-Brexit period, sterling-denominated loans comprised around 70% of the UK-based syndicated loan market. But the share has continuously decreased since 2015, plummeting to less than 10% in 2022.

Source: Debtwire

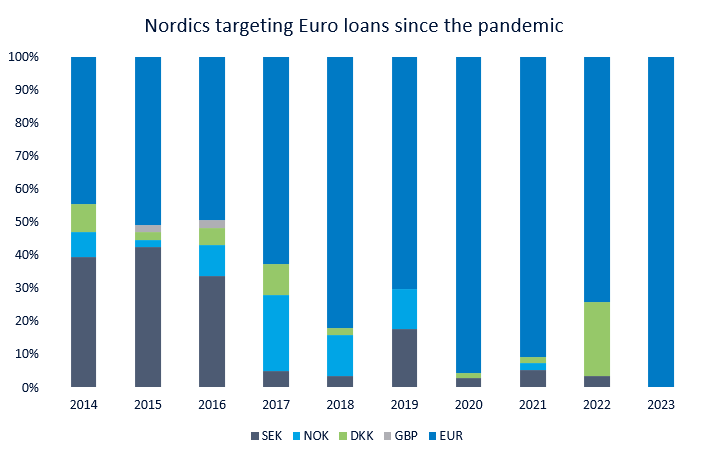

In the Nordic countries, the decrease in local currency denominated loans issued in Norwegian, Swedish, and Danish is less linear but still palpable. Issuers from Norway, Sweden and Denmark used to print 50% to 60% of their deals in their local currencies up to 2016, a figure that has dropped significantly during the pandemic.

In 2022, companies such as SSI, BoConcept and Carousel Logistics issued a combined EUR 300m-equivalent loans denominated in DKK, causing a jump in the local currency share to 26% of the total market. However, it appears to have been a temporary outlier, as thus far, in 2023, no Nordic institutional loans denominated in krone have come to the syndicated European market.

Source: Debtwire

Leveraged loan investors favour euro-denominated instruments in the current environment due to a decrease in both currency and liquidity risk caused by a deeper investor base. This move has cemented the gradual domination of the euro, which was spurred on over the years by the maturation of the CLO market and the weakening of the sterling investor base.

A service of

Start your trial. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in