DebtDynamics EMEA | Kicking the can: refinancing and extensions dominate issuance and hit highest share in a decade

Source: Debtwire

Lack of new money

The high interest rate environment and the uncertainty surrounding peaks, means there is little-to-no incentive for new money deals, giving way to a flurry of refinancings.

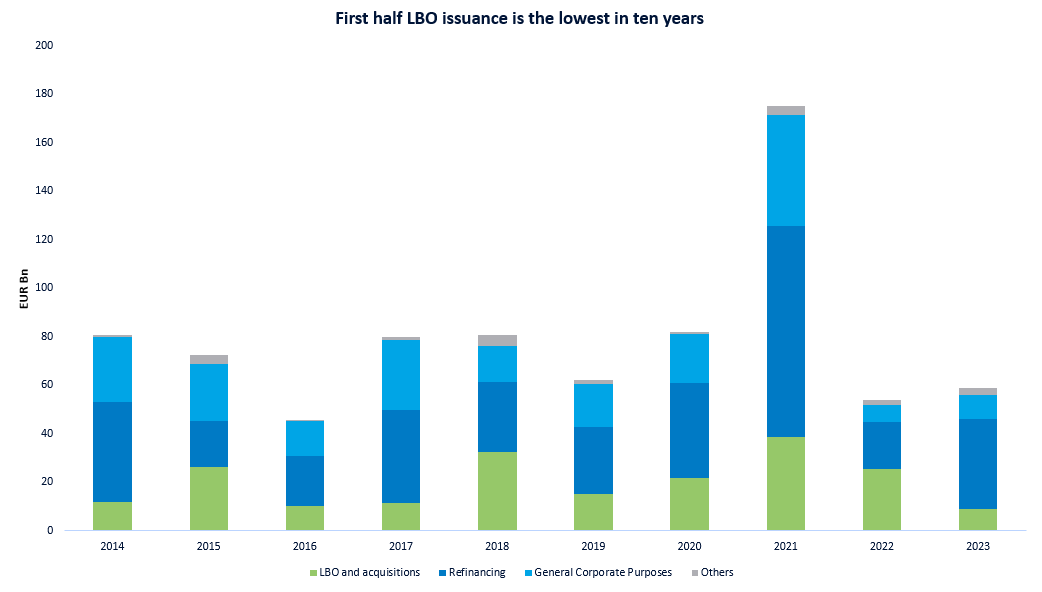

The figures show how hard it’s been for investment bankers to bring new money to the market, with the financing of leveraged buyouts and acquisitions funded by term loan Bs and corporate high-yield bonds dropping to their lowest level in a decade. And this is true for both the amount issued and the market share.

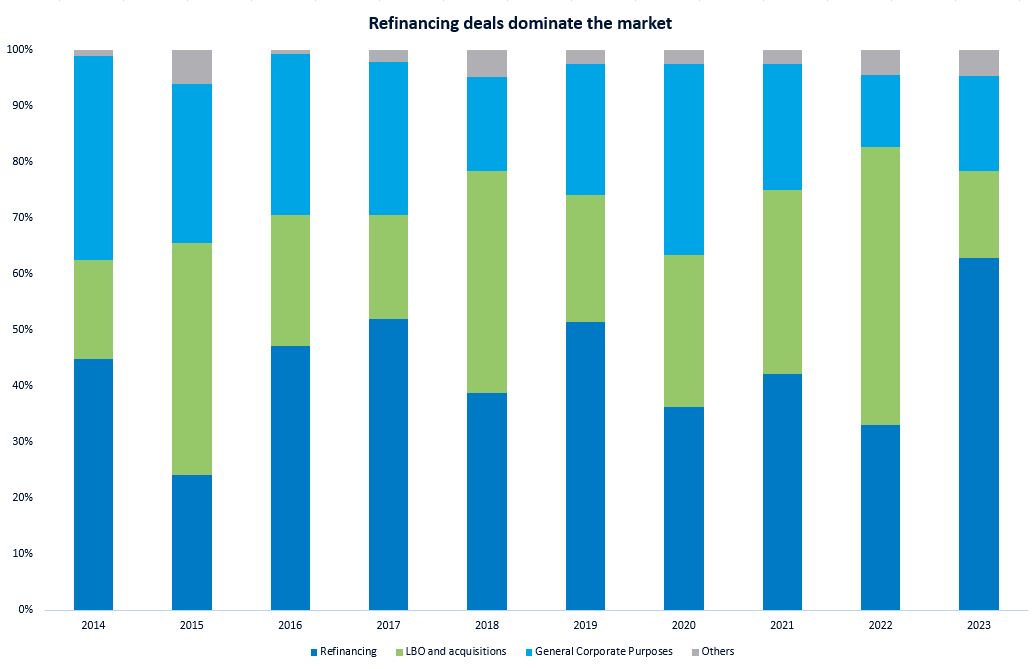

Issuances to finance LBO and acquisitions YTD made up just 15.5% of the total printed, a fraction of the 49% peak of 2022 and significantly lower than the 29% average of the past decade. In volume, the EUR 9.13bn issued thus far to finance buyouts and acquisitions is the lowest amount compared to other first semesters since 2014.

Source: Debtwire

While the total amount issued in 2023 (EUR 58.8bn) came in below the first-halves’ average of EUR 79.2bn, the effect was particularly noted among new-money transactions, with LBO and acquisition funding amounting to less than half of the historical average of EUR 20.2bn.

The LBO TLB boom aftermath

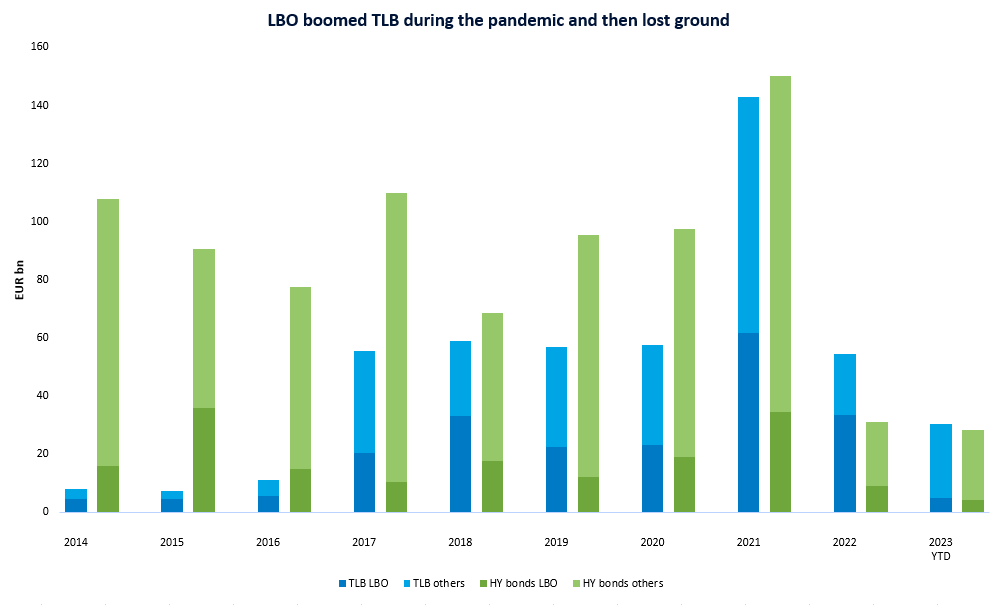

When split between loans and bonds, LBO issuance as a share of the total is relatively stable on the bond side when compared to the much more volatile TLB market. High-yield bonds to fund buyouts and acquisitions have ranged from 6.2% and 13.7% since 2017. The TLB LBO market has been like a roller coaster, with this year’s figure (8.5%) well below last year’s 39.2%.

Focusing on the nominal amounts issued, the decrease is again much more prominent in loans, the primary tool used in previous years, when the LBOs had their boom.

In 2021, EUR 61.7bn worth of term loan B facilities was printed to finance acquisitions. The figure dropped by nearly half in 2022 and has yet to reach EUR 9bn in 2023 so far.

Source: Debtwire

The chart shows that, beyond the decrease in total issuance, there’s a more substantial fall in debt to fund LBOs and an even more dramatic drop among TLB facilities in which the primary use of proceeds is to fund buyouts and acquisitions. This retreat has made room for the current situation in the levfin market, dominated by refinancing, amendments and extensions issued by companies with an urgent need to push deadlines.

A service of

Start your trial. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in