Curo Group Holdings Corp – Sale of Flexiti to provide liquidity support – 2Q23 Credit Report

Overview

Curo Group Holdings Corp. (NYSE: CURO) is a non-bank lender. The company offers products and services to consumers in the US and Canada.

Recent Events

On 3 August 2023, CURO released 2Q23 results before market open. Reported revenue of USD 209.2m narrowly missed estimates for USD 209.8m. CURO also announced it has entered into an agreement to sell the Flexiti business and expects to net proceeds in the range of USD 50m to USD 60m from the sale, which is expected to close in September 2023. CURO stock traded down as much as ~12.5% in the 3 August 2023 session and is down ~9% since the release. The company’s 1.5 Lien 7 1/2s of 2028 are also up ~1.5points since the release.

Financials

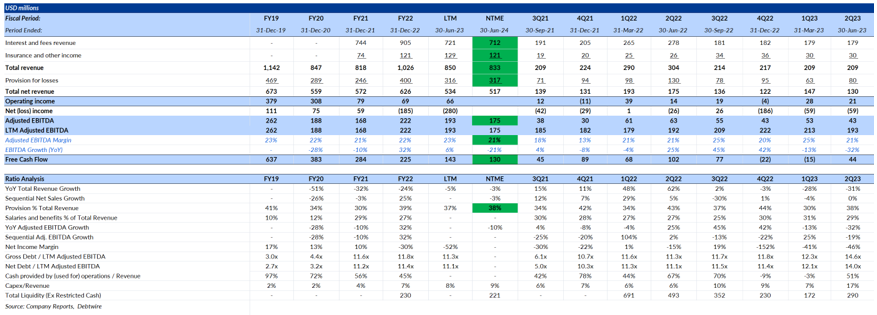

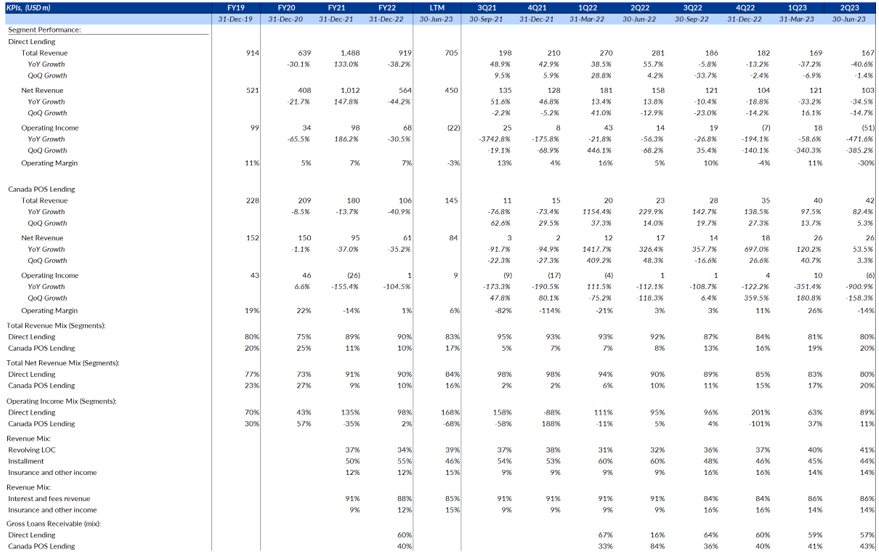

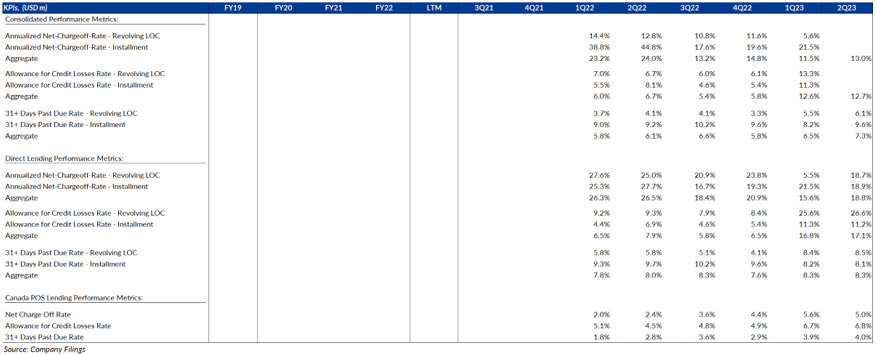

CURO reported revenue of USD 209m for 2Q23, versus USD 304m for 2Q22, a decrease of 31% YoY. Direct Lending revenue was USD 167m for 2Q23, versus USD 281m for 2Q22, a decrease of ~41%. This segment represented approximately 80% of CURO’s revenue for 2Q23. Consistent with prior period comments, management noted the YoY decline was due to a strategic shift towards a higher mix of longer-term, lower yield and lower risk products in this segment. The small yet growing Canada POS segment posted USD 42m in revenue for 2Q23, versus USD 23m in 2Q22, representing impressive ~82% YoY growth. Overall, management noted that they have not seen any “unusual consumer stress” and feel that the credit environment for their business remains stable.

Operating margin for 2Q23 was 10%, versus 5% in 2Q22. Current provisions were 38% of revenue for 2Q23, below the 43% of revenue level in the prior year period. Salaries and benefits increased to 29% of revenue in 2Q23 from 27% in 1Q22. CURO reduced advertising spend meaningfully in 2Q23 (USD 2m versus USD 13m in the same period last year), consistent with its pivot to slower more focused growth. The company noted on the 2Q23 call that they expect marketing spend to increase into 2H23.

Adj. EBITDA for 2Q23 was USD 43m versus USD 63m for 2Q22, driven mainly by the absence of various add-backs in 2Q23. Free cash flow for 2Q23 was USD 44m versus USD 102m in 2Q22, driven by lower receipt of fees and interest payments and flat capex spend YoY.

CURO is significantly levered. Management has set a goal to reduce leverage to the range of 5x to 6x ahead of the August 2027 Term Loan maturity. The company is also pivoting towards longer-duration, lower-rate secured products, for example, loans secured by customer vehicles which management mentioned on the 2Q23 call as forthcoming sometime in FY2023. This should be a less volatile strategy, which should provide comfort to the various lenders. CURO still needs to grow its way into its capital structure over the next several years.

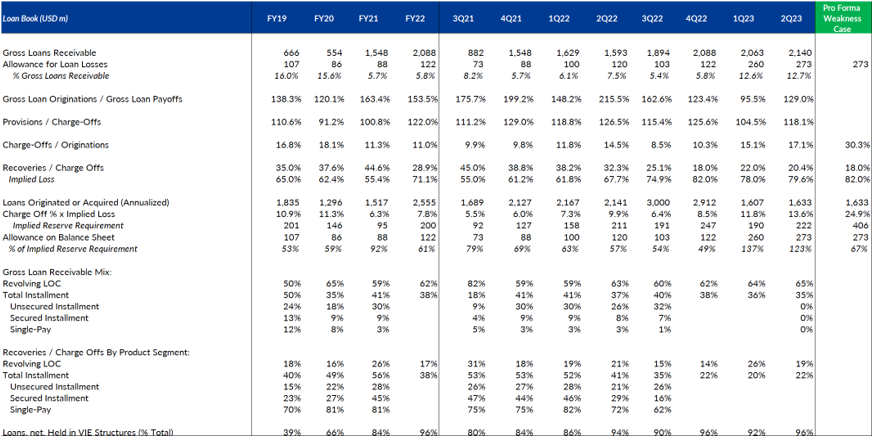

Debtwire’s NTM estimates take into account recent company guidance for gross loan book growth as well our estimates for recent yield and margin trends. We have assumed 8% overall growth in the book and an annual yield of 32%, based on our analysis of CURO’s loan book. Potential drivers of upside from our estimates include higher growth in the loan book, higher yield from the loan book and lower provisions. Potential drivers of downside include lower yield from the loan book as management pivots the business to lower rate products and higher provisions if credit conditions weaken. Note that our 32% yield is 200bps lower than our estimated 2Q23 levels and reflects our current estimate for impact from the previously mentioned strategic shift.

The following table highlights CURO’s loan book and our analysis of an estimated downside case. While credit quality appears stable based on recent results and comments on the 2Q23 call, we estimate that the company could face a USD 130m+ special provision / charge in a downside scenario, meaningful if only as this would eat up more than 60% of our estimated liquidity as of 30 June 2024, which would remain positive at an estimated USD 87m. In this analysis we have assumed CURO’s book gets hit on all sides: (i) Charge-Offs / Originations hit 2Q20 levels (recent highs); and (ii) Recoveries / Charge Offs hit 4Q22 levels (recent lows). We are not forecasting this outcome, and instead share the analysis in order to contextualize potential risk in a downside scenario.

Valuation

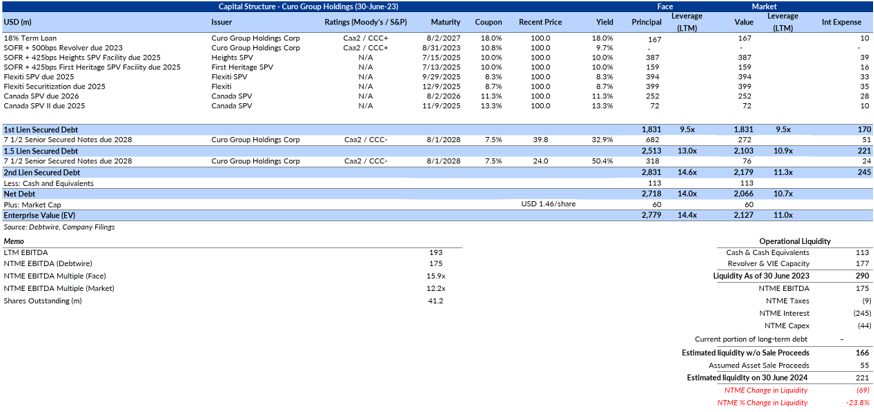

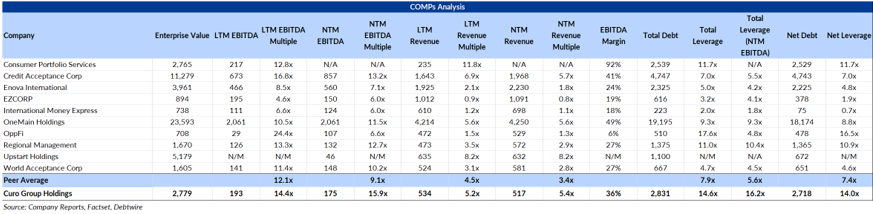

CURO is currently trading at an LTM EV/EBITDA multiple of 14.4x, versus a peer average of 12.1x. NTME multiple is 15.9x, versus a peer average of 9.1x. The company’s LTM EV/Revenue multiple is 5.2x versus a peer average of 4.5x. NTME multiple is 5.4x, versus a peer average of 3.4x. Total leverage is 14.6x, and Net leverage is 14.0x versus a peer average of 7.9x and 7.4x. CURO’s Total Leverage based on NTM EBITDA stands at 16.2x versus a peer average of 5.6x. Traditionally we would look to value a financial concern like CURO based on book value. This is not possible given a negative balance.

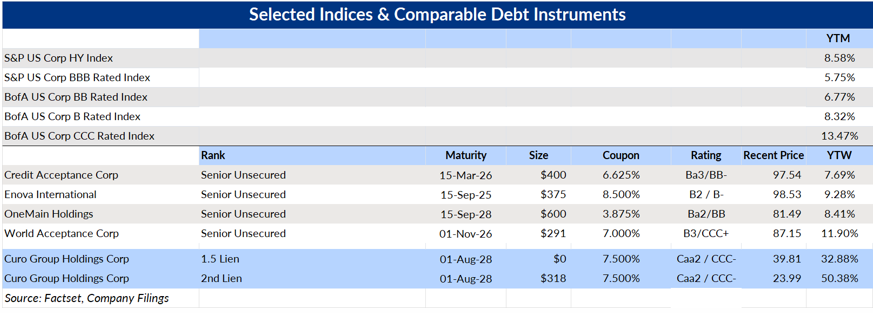

CURO’s 1.5 lien 7½% Senior Secured Notes and 2nd lien 7½% Senior Secured Notes both trade along with the equity. Based on our liquidation analysis, the 2nd lien paper remains overvalued versus recent prices. The 1.5 lien paper is potentially a more attractive trade. Based on our mid-point liquidation value of 50, current pricing suggests a potential ~47% YTM assuming a liquidation is completed on 1 August 2025. Given recovery expectations, we believe the spread between the 1.5 lien and 2nd lien should also widen, making it potentially compelling to explore a capital structure trade, especially as the two pieces of paper carry the same coupon (the trade then self finances, excluding cost to borrow the 2nd lien paper for the short leg of a trade). The Term Loan is also worth watching if it begins trading as it should be well covered even if the loan book melts down completely. CURO will likely opt for the PIK feature, at least in the near term.

CURO’s equity is also dollar cheap at recent prices (USD 1.46/share) but rich to the comparables on a multiples basis. The equity represents a tiny sliver in CURO’s USD ~2.8bn capital stack. While it is likely worthless based on our analysis, it is a relatively better bet than the 2nd Lien paper for parties playing contrarian, as the 2nd lien paper should trade at a meaningful spread to the Term Loan and 1.5 lien facility given the most junior priority / lien status.

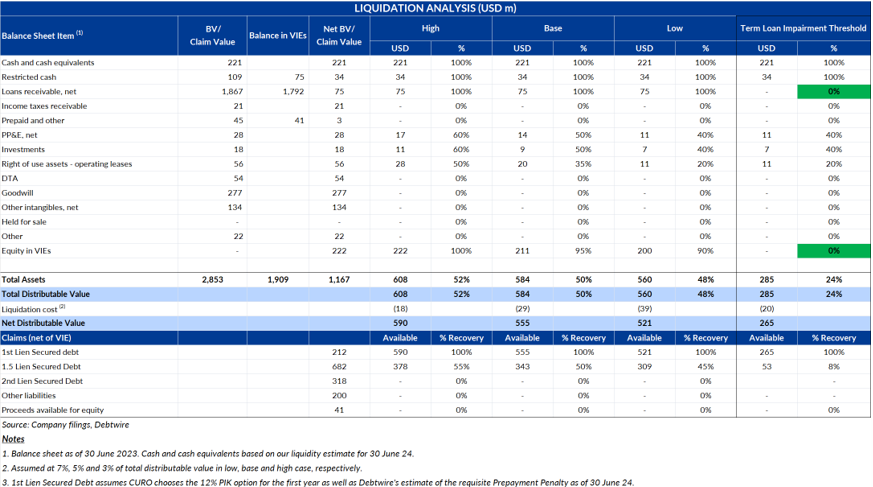

A high-level liquidation analysis of CURO suggests the company’s 1st Lien debt is well covered. All else being equal, we believe the loan book (and Equity in VIEs, which is a derivative of the loan book estimate) can be marked down to zero value and the term loan is still covered. Based on our analysis and estimates, the 1.5 lien debt is meaningfully impaired, and the 2nd lien debt looks to be worthless, along with the equity.

A service of

Start your trial. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in