CASE PROFILE: SmileDirectClub aims for 60-day sale process, exit from Chapter 11 by end of 2023

SmileDirectClub (SDC), with nearly USD 1bn in funded debt, filed for Chapter 11 on Friday (29 September) with plans to sell its assets over the next two months.

The orthodontics company’s bankruptcy petition follows years of net losses amid a confluence of factors, including the coronavirus pandemic. Funded with USD 80m in debtor-in-possession (DIP) financing, SDC will head to court this afternoon (2 October) for a first day hearing before Judge Christopher Lopez of the US Bankruptcy Court for the Southern District of Texas.

Debtwire Dockets: SmileDirectClub Inc

The company

Founded in 2014, the company is a Dental Support Organization with a business model based on keeping down consumer orthodontic costs compared to its peers, according to court documents.

SDC saw strong growth in its early years, with USD 20.6m in revenue in 2016 and USD 750m in 2019. As of the petition date, the company has 110 SmileShop retail locations in the US plus operations in Canada, UK, Australia, Costa Rica, and Ireland. Prior to the pandemic, SmileShop stores accounted for 90% of the company’s revenue, with the remaining 10% coming from its telehealth model.

The company has a manufacturing facility in Antioch, Tennessee, with 300 employees.

The debt

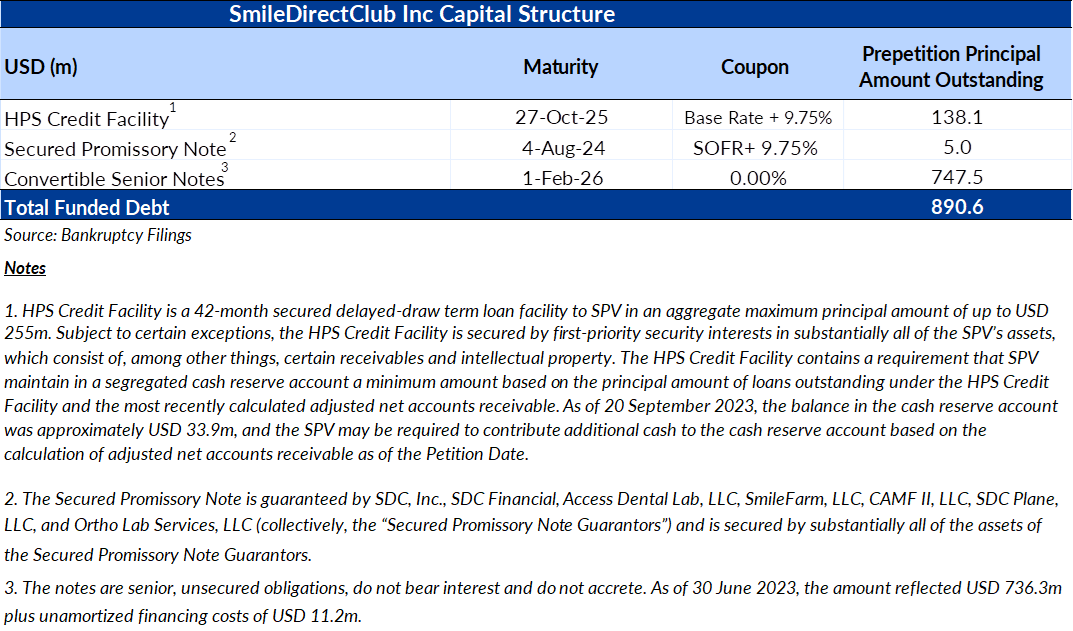

SDC enters Chapter 11 with USD 890.6m in funded debt. The first of that financing came in February 2021, when the company issued USD 747.5m in 0% convertible unsecured senior notes due 2026. At the same time, the company raised USD 97.5m in incremental financing.

In April 2022, SDC brought in another USD 138.1m on a credit facility led by HPS Investment Partners and various lenders, priced at the base rate plus 9.75% and maturing October 2025.

The descent

As discretionary consumer spending decreased as the pandemic dragged on, SDC faced store closures, supply chain disruptions, labor shortages, and a reduced ability to fulfill orders, according to the first day declaration of Chief Financial Officer Troy Crawford.

The company shifted its in-store model to doctor-prescribed impression kits that SDC shipped to customers’ homes. The shift led to a decrease in revenue and the company saw a net loss of USD 278m in 2020, USD 335.7m in 2021, and USD 277.9m in 2022, with an overall drop of 37.3% from 2019 to 2022, according to Crawford’s declaration.

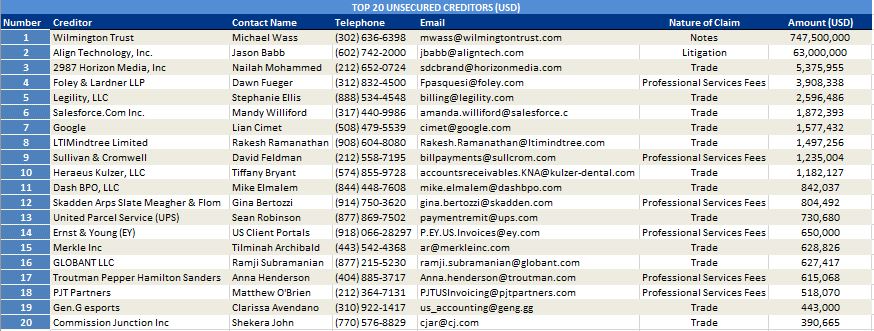

Those issues were complicated by long-running litigation with Align Technology Inc, the maker of Invisalign and the debtor’s largest competitor. Align acquired a 17% equity interest in the company in 2016 – later increased to 19% – and became SDC’s exclusive third-party supplier of aligners. But the deal fell apart and an arbitrator found in 2019 that Align had violated the terms of the agreement by modeling itself on SDC’s model and trying to compete with the company and ordered Align to close its retail locations and cancel its ownership stake. The tables have turned since then, with Align launching an arbitration proceeding before the American Arbitration Association, which issued a final award of USD 63m in favor of Align in May 2023, confirmed by the California Superior Court on 12 September. That order gave SDC 60 days to appeal the decision and stayed Align from acting on the judgment until 29 September, but SDC filed for Chapter 11 that day.

SDC also faces several shareholder and non-shareholder class actions alleging that the company made inaccurate and misleading statements as part of its initial public offering.

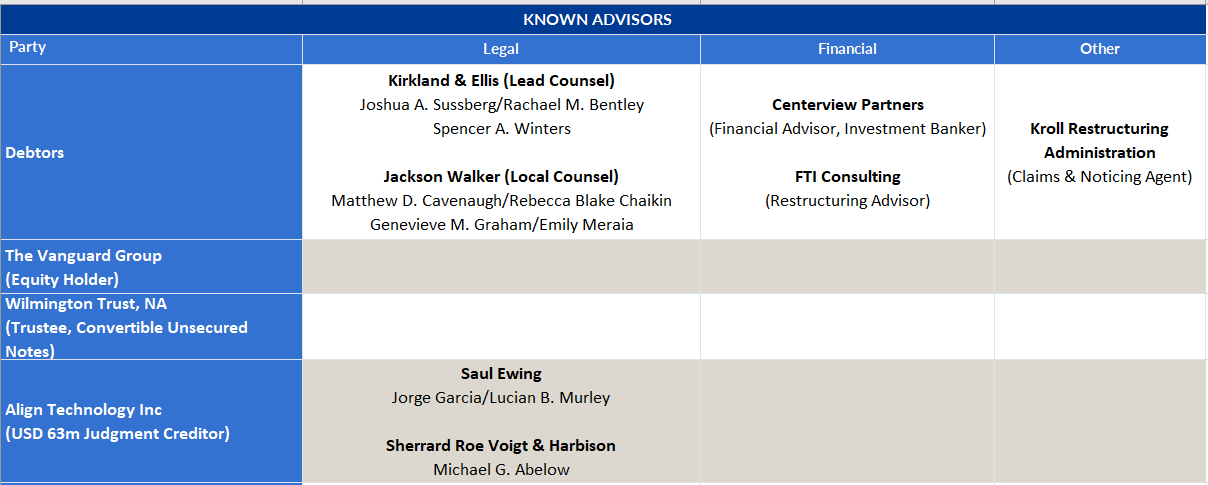

Amid those troubles, SDC hired a roster of advisors including FTI Consulting, Kirkland & Ellis and Centerview Partners and entered talks with a group of convertible noteholders represented by Latham & Watkins, and a group of convertible noteholders that hired Paul Weiss Rifkind Wharton & Garrison and Ducera Partners. Centerview launched a search for financing but did not find any actionable proposals, according to the declaration.

Unable to raise new debt and coming up against the expiration of the stay period against Align, SDC elected to file for Chapter 11 to pursue a sale of its assets.

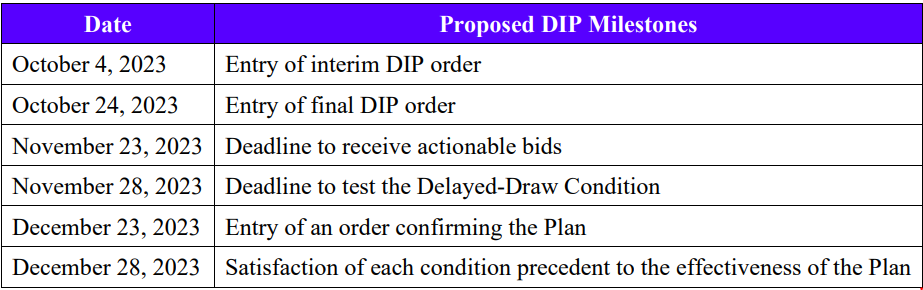

The DIP and the sale

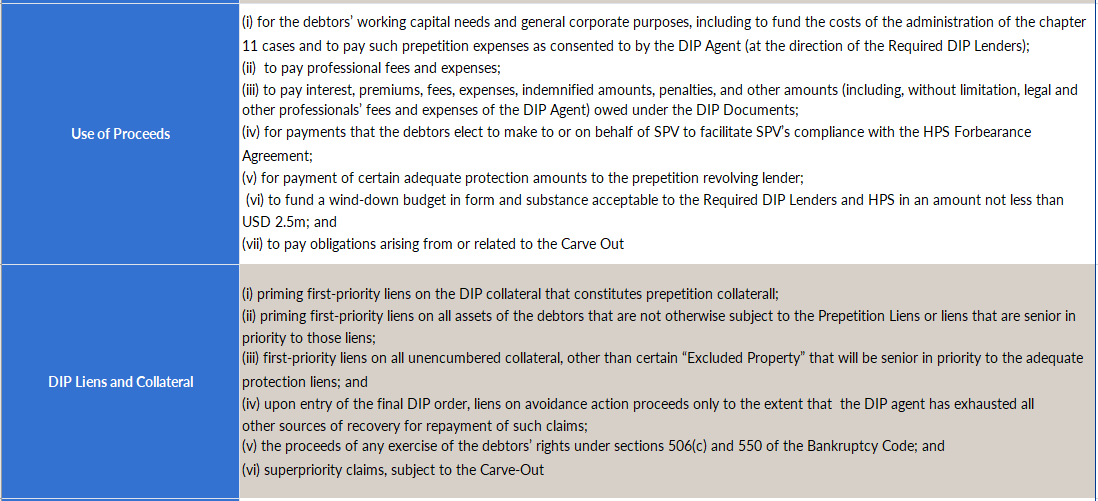

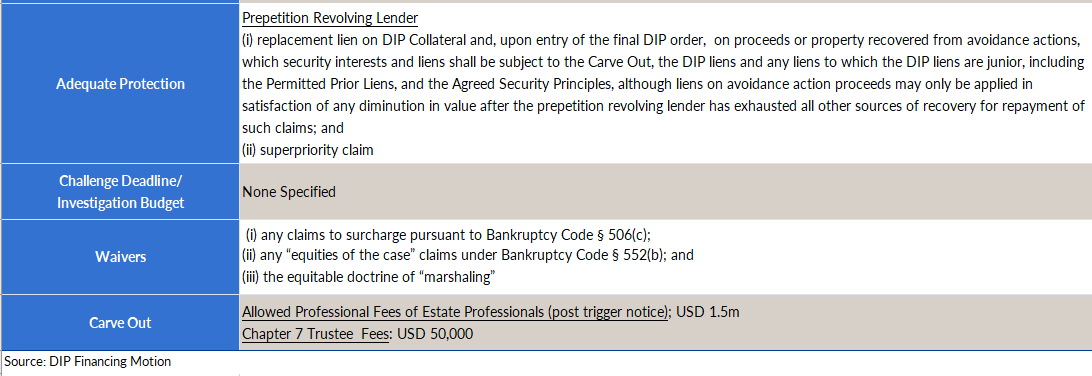

The company has lined up an USD 80m DIP to fund the sale process, consisting of USD 20m available on an interim basis, a USD 30m delayed draw, a USD 25m accordion, and a USD 5m rollup of a prepetition promissory note.

The DIP sets a series of milestones for the case, including a 23 November bid deadline, 23 December plan confirmation deadline, and 28 December deadline to put the plan into effect. If the company is unable to line up a deal, it would pivot to a liquidation under a Chapter 11 plan.

The advisors

A service of

Start your trial. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in