CASE PROFILE: Air Methods kicks off Chapter 11 with lender, noteholder-backed plan to cut debt

Air Methods Corp, an emergency medical transportation company, filed for Chapter 11 early this morning (24 October) with a plan of reorganization backed by a majority of its secured lenders and unsecured noteholders.

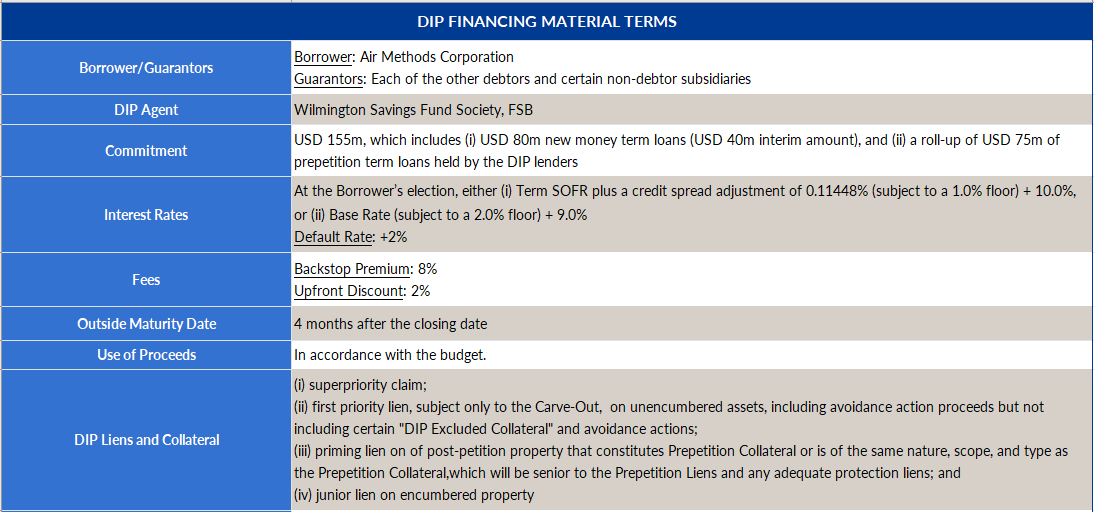

The plan proposes to leave unsecured creditors unimpaired while continuing to service hundreds of millions of dollars in aircraft financing agreements. The plan would cancel the rest of the company’s prepetition debt in favor of rights to participate in a USD 135m rights offering and new USD 250m first lien exit term loan. Certain prepetition creditors have agreed to backstop USD 155m in debtor-in-possession (DIP) financing to fund the case.

The company aims to complete the case in six weeks, proposing a 4 December plan confirmation. But first, Air Methods will head to court this afternoon for its first day hearing at 2:30pm CT before Judge Marvin Isgur of the US Bankruptcy Court for the Southern District of Texas.

Debtwire Dockets: Air Methods Corp

The company

Founded in 1980, Air Methods is a provider of air medical emergency services from 275 bases in 47 US states. The Greenwood Village, Colorado-based company has a fleet of 390 helicopters and fixed-wing aircraft. As of the petition date, the company had 4,900 employees.

In addition to those medical services, the company designs and manufactures aeromedical and aerospace technology that it sells to third parties consisting primarily of governmental clients, according to court documents.

Via non-debtor entities, the company operates Blue Hawaiian, a provider of helicopter tours and charter flights in Hawaii.

American Securities LLC and affiliates acquired Air Methods in 2017 for USD 2.5bn. As of the petition date, American Securities holds 94.7% of the company’s equity. At the time of the acquisition, the company entered its existing prepetition credit agreement and unsecured notes, loading it with more than USD 2bn in funded debt.

The debt

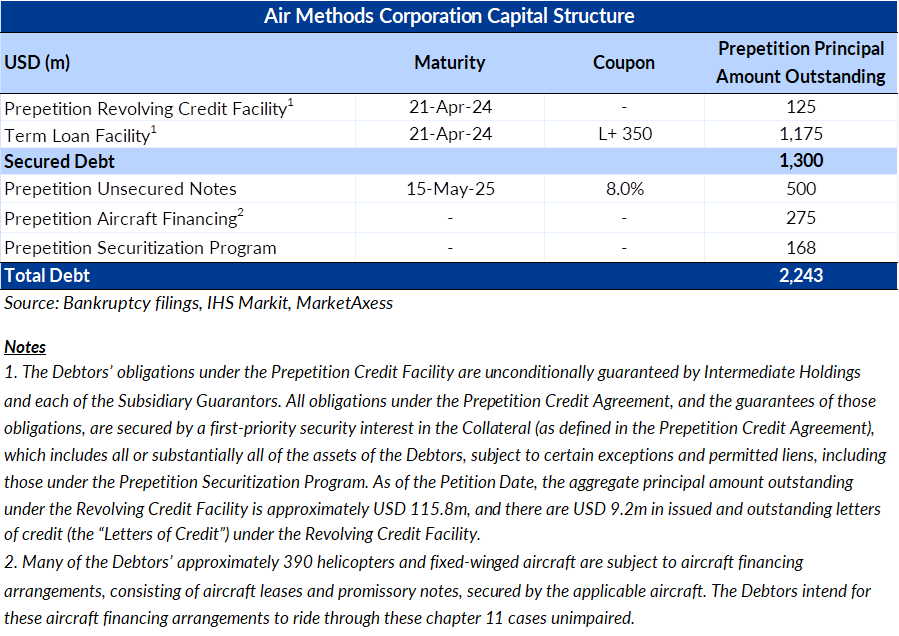

That USD 2.24bn funded debt load stems primarily from a 2017 credit agreement with various lenders and Royal Bank of Canada as administrative agent. Air Methods owes USD 115.8m on a revolver and USD 1.18bn on the term loan portion of the facility, both set to mature in April 2024.

The debtor also has USD 500m in 8% unsecured notes outstanding, due 2025.

Beyond the credit facility and notes, Air Methods has USD 275m in aircraft financing and USD 168m in securitization programs.

The descent

While the American Securities deal provided “much-needed” capital, that debt load has become unsustainable, according to the first day declaration of interim CEO Jason Kahn. A tight labor market led the company to “significantly increase” employee compensation, and operating costs have generally risen amid inflation.

The interim chief also pointed to the 2022 implementation of the No Surprises Act, which established federal protections against surprise medical bills. That created “red tape” for the company, delaying the company from bringing in receivables amid dispute resolution processes and a shortage of arbitrators, Kahn claimed.

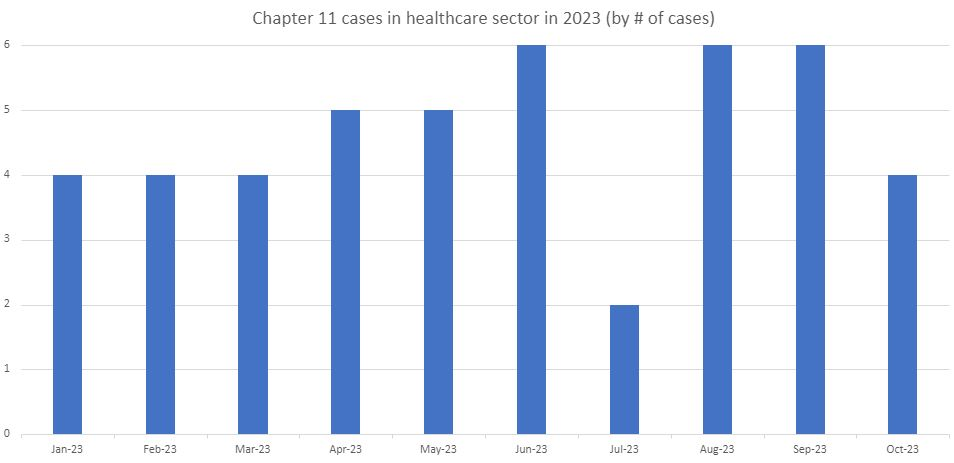

This has been a heavy year in Chapter 11 for healthcare providers or healthcare-adjacent companies, with more than one per week through 24 October 2023, according to Debtwire’s Restructuring Database.

Source: Debtwire Restructuring Database

Air Methods implemented an operational turnaround in 2019, improving its sourcing and closing underperforming bases, but still needs to restructure its debt load amid upcoming maturities on the debt. The company started bringing on a roster of advisors late last year, hiring Weil Gotshal & Manges as legal counsel and Lazard as financial advisor to explore strategic alternatives, and followed up in January 2023 by forming a special committee with three independent directors.

Earlier this year, the company engaged an ad hoc group of lenders, represented by Davis Polk & Wardwell and Evercore, to determine a way forward. The parties entered a restructuring support agreement on Monday (23 October) and filed for Chapter 11 the next day with a prepackaged plan in hand. The proposal is backed by holders of 71.6% of the prepetition credit facility, 66.8% of the unsecured notes, and American Securities.

The DIP and the plan

Certain members of the ad hoc group have agreed to fund the case with USD 155m in DIP financing consisting of USD 80m in new money and a USD 75m rollup of prepetition term loans. The DIP would roll into an exit facility.

Under the plan, the company’s aircraft financing debt and general unsecured creditors will be unimpaired.

Lenders on the prepetition credit facility, for claims other than the DIP, would see an estimated 16% recovery via rights to subscribe to USD 200m of the USD 250m new first lien exit term loan and rights to participate pro rata in the USD 135m rights offering. The lenders could instead elect to receive cash for their claims.

Unsecured noteholders are expected to see a recovery of 1% via a USD 500,000 cash pool, Tranche 1 warrants for up to 10% of new common stock and Tranche 2 warrants for up to 5% of common stock. The noteholders, like the prepetition lenders, have the option to cash out instead.

The restructuring agreement sets a six-week timeline for the case, proposing a 4 December plan confirmation hearing.

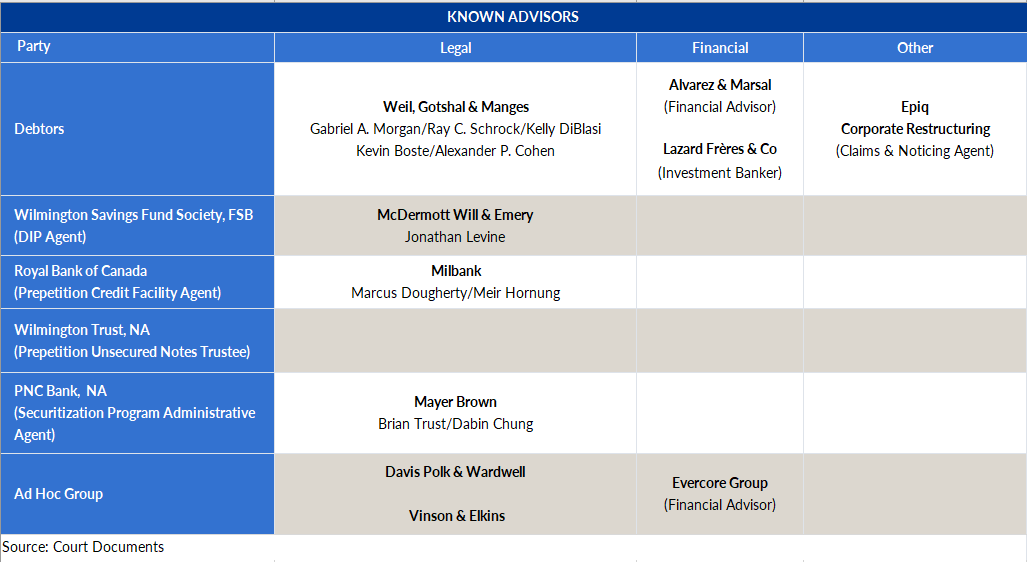

The advisors

A service of

Start your trial. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in