Carvana’s restructuring path: potential speedbumps and benefits under a Chapter 11 scenario

by Sara M. Tapinekis and Kaushal Mehta

Carvana Co, an Arizona-based e-commerce platform for buying and selling used cars, has been taking steps to address the fact that, as Debtwire reported, the company’s liquidity (excluding unpledged assets of USD 2bn) has declined for last three quarters. The company launched a debt exchange offer to extend certain maturities and reduce its funded debt, which the company has extended several times (most recently on 17 May). However, the offer reportedly has met resistance from a bondholder group holding a significant portion of Carvana’s senior unsecured notes, which are the subject of the exchange offer. In this article, Debtwire’s legal analyst team discusses the potential impact a Chapter 11 filing could have on Carvana’s restructuring efforts if the company were to decide to shift gears and seek bankruptcy protection.

Putting purchasers in the driver seat – eliminating the salesperson

Through its website, Carvana.com, Carvana provides an online process for purchasing a vehicle with features including a seven-day money back guarantee, home delivery, and a nationwide inventory selection. Not only can Carvana’s customers purchase vehicles without going through a salesperson, they can also purchase vehicle service contracts and auto insurance on the company’s website.

To further facilitate the process, Carvana originates loans for its customers and sells them to partners and investors pursuant to finance receivable sale agreements. In December 2016, Carvana entered into a master purchase and sale agreement (MPSA) with Ally Bank and Ally Financial Inc, pursuant to which it sells finance receivables meeting certain underwriting criteria without recourse to the company for their post-sale performance. Pursuant to the MPSA, which has a 12 January 2024 scheduled commitment termination date, the Ally parties committed to purchase up to a maximum of USD 4bn of principal balances of finance receivables between 13 January 2023 and the scheduled commitment termination date.[1]

In addition to purchases, Carvana also offers customers the option to sell or trade-in vehicles at any of its locations, including its patented car vending machines, in over 300 US markets, according to the company’s Form 8-K dated 17 May. The company boasts that it is the number two automotive brand in the US, second only to Ford.

Carvana Co. is a holding company that was formed as a Delaware corporation on 29 November 2016 to complete its initial public offering and operate the business of Carvana Group, LLC and its subsidiaries (collectively, the Carvana Group). According to Carvana’s Quarterly Report filed on 4 May, substantially all of the company’s assets and liabilities are assets and liabilities of the entire Carvana Group, except the senior notes, which were issued by Carvana Co and are guaranteed by its and Carvana Group’s existing domestic restricted subsidiaries, excluding ADESA US Auction, LLC and its subsidiaries, which Carvana designated as unrestricted subsidiaries under the relevant indentures in March 2023.

There are five series of senior unsecured notes, which include the: (i) 2025 senior unsecured notes due 1 October 2025 (2025 Notes); (ii) 2027 senior unsecured notes due 15 April 2027 (2027 Notes); (iii) 2028 senior unsecured notes due 1 October 2028 (2028 Notes); (iv) 2029 senior unsecured notes due 1 September 2029 (2029 Notes); and (v) 2030 senior unsecured notes due 1 May 2030 (2030 Notes). US Bank NA is the senior unsecured notes trustee.

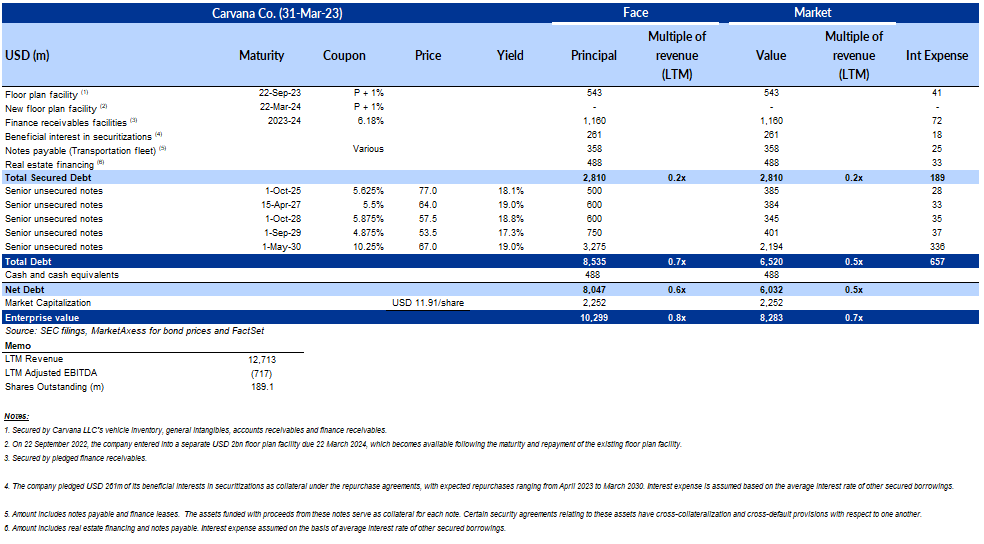

In addition to over USD 5.6bn outstanding in senior unsecured notes, the company also has floor plan facilities to finance its vehicle inventory and finance receivable facilities, which are short-term revolving credit facilities. The proceeds of these facilities fund certain finance receivables originated by Carvana prior to selling them. The company’s capital structure is summarized in the table below.

Out of court restructuring efforts

Carvana stated in its Quarterly Report that it has incurred losses since its inception and expects to incur additional losses. In its 4Q22 letter to shareholders (dated 23 February), the company explained that “[a]fter the pandemic, snarled automotive supply chains and historically rapidly rising interest rates combined to dramatically impact the affordability of used cars.” To address these and other headwinds, the company stated that it intends to reduce both its inventory and its advertising budget. With respect to servicing its funded debt, the company hopes to extend the maturity date of its facilities within the next year by amending its existing facilities or entering into new agreements.

Also, on 22 March, Carvana launched an exchange offer for holders of its senior unsecured notes, offering them the option to exchange their notes at a discount for up to a principal amount of new USD 1bn 9% (or 12% PIK toggle) senior secured second lien notes due 2028. The offer was set to expire on 19 April, but the company extended the deadline to 3 May and sought to entice noteholders by offering an early exchange premium and an increase in exchange consideration for 2025 Notes. The offer was extended again – this time to 17 May – and then on 17 May, the company amended its offer again, extending the deadline to 1 June. This time, the company offered an early exchange premium of USD 20 per USD 1,000 principal amount of existing senior notes. Thus, the total consideration per USD 1,000 principal amount of existing senior notes tendered would be (i) for the 2025 Notes – USD 858.75; (ii) for the 2027 Notes – USD 658.75; (iii) for the 2028 Notes – USD 646.25; (iv) for the 2029 Notes – USD 632.50; and (v) for the 2030 Notes – USD 793.75.

Carvana’s challenges and the road ahead

As Debtwire previously reported, Carvana’s net loss for the year reached USD 2.894bn and the company has been talking about a potential restructuring with Kirkland & Ellis and Moelis. However, it also was reported in March that a group holding a significant portion of the senior unsecured notes had opposed the company’s proposed restructuring.

In addition to concerns about refinancing its existing funded debt, Carvana has also faced complaints from its vehicle-purchasing customers who have alleged that Carvana failed to timely provide titles to the vehicles they purchased in accordance with the applicable state law. In 2021, for example, two individuals in Pennsylvania filed a putative class action complaint alleging that although they paid state registration and license plate fees to Carvana, the car dealer failed to complete the permanent registration of their vehicles and provided only temporary license tags without the legal right or authorization to do so. The plaintiffs asserted breach of contract claims and that Carvana violated Pennsylvania’s Unfair Trade Practices and Consumer Protection Law. In January 2022, Carvana moved to dismiss the case and compel arbitration, arguing that the contracts entered into by the parties – retail purchase agreements (RPAs) – contain binding arbitration provisions on a non-class basis. Put simply, Carvana argued that through arbitration agreements incorporated into the RPAs, the plaintiffs waived the right to a class action or private attorney general action and agreed to submit their disputes to arbitration.

After hearing oral argument in June, the US District Court for the Eastern District of Pennsylvania denied Carvana’s motion. In October, Carvana appealed that ruling to the US Court of Appeals for the Third Circuit. That appeal is pending and the action in the District Court is stayed during the pendency of the appeal. Most recently, on 18 April, Carvana filed a request for oral argument with the Third Circuit appellate court, arguing that the issue on appeal is a matter of first impression that will significantly impact Carvana’s business. The issue concerns the enforceability of the arbitration agreements under Pennsylvania’s Motor Vehicle Sales Finance Act (MVSFA). According to Carvana, neither the appellate court nor the Pennsylvania Supreme Court “has addressed whether the MVSFA requires all agreements between an installment buyer and seller, including non-financing terms, to be contained in a single document, rather than in a single contract comprised of multiple documents incorporated by reference into one another.” Carvana is represented in that action by Latham & Watkins and Kleinbard.

While the commencement of a Chapter 11 case would offer Carvana a breathing spell from similar customer actions[2] due to the triggering of the automatic stay, it also would provide a single forum for the company to address these claims. If Carvana is unsuccessful on its appeal, the automatic stay may become an even greater enticement.

With respect to the company’s efforts to exchange its senior unsecured notes for second lien notes, it is unclear whether Carvana will extend the 1 June offer deadline. While that decision may largely depend on the progress of discussions with the bondholder group, it is unclear what portion of the senior notes the group controls. If Carvana sought to accomplish a similar restructuring in Chapter 11, in order to have an accepting class under a Chapter 11 plan, it would need a buy in from holders of two-thirds in amount and over half in number. Alternatively, a group holding at least 34% of the notes could block an accepting class vote. If, on the other hand, Carvana were able to obtain at least one impaired class of creditors that voted to accept its Chapter 11 plan, it could opt to cram down the senior unsecured noteholders. To do so, its plan must (i) not discriminate unfairly against the noteholders and (ii) be “fair and equitable” to them. To meet the latter requirement, a Chapter 11 plan must comply with the “absolute priority rule,” meaning that it must not provide a distribution to a junior creditor before the noteholders are paid in full (eg – equity would be wiped out). The plan also must provide that the noteholders, if crammed down, would receive distributions that are not less than the amount that the noteholders would have received if Carvana were to be liquidated under Chapter 7 of the US Bankruptcy Code. According to Debtwire’s recent credit report for the company, in a liquidation scenario, holders of the senior unsecured notes would see a recovery ranging between 19% and 53%.

If, on the other hand, completing the debt exchange offer is insufficient to adequately restructure the company’s debt and Carvana decides to pursue a Chapter 11 filing after completing the exchange offer to achieve a more comprehensive restructuring, it could face risk related to the exchange offer if a disgruntled group of non-participating noteholders looks to challenge the exchange. Serta Simmons Bedding (SSB) is a prime – and ongoing – example. In that case, prior to the bankruptcy filing, SSB and a group of priority term loan (PTL) lenders agreed to a financing and debt exchange transaction that restructured certain of the company’s debt by creating a new superpriority position. That position included USD 200m of new loans originated by the PTL lenders, plus USD 875m issued to them in exchange for a greater amount of their first and second lien loans. The non-participating lenders (non-PTLs) that were left subordinated argued that the transaction violated the terms of their credit agreement with SSB,[3] and that the actions of the company and its supporting PTLs breached their implied duties of good faith and fair dealing. Although the Bankruptcy Court ultimately ruled against the non-PTLs on their contract claim, the fight over whether SSB and the PTL lenders breached an implied covenant of good faith and fair dealing has seeped into SSB’s contested confirmation hearing,[4] which spanned five days with the court taking the matter under advisement. On the fourth day of the hearing, SSB’s counsel stated “[w]ith all due respect . . . [the non-PTL lenders] have one goal, which is to blow up our plan.” While the debt exchanges are not structurally similar and any associated legal issues associated arising from the exchanges would differ, the case serves as an example of the extent to which disgruntled non-participating prepetition lenders can disrupt and delay confirmation. While this should not serve as a deterrent to a Chapter 11 filing following a debt exchange, it should, at minimum, serve as a warning and potential risk to avoid during any prepetition lender negotiations.

The Debtwire team will continue to monitor the situation.

———-

[1] According to the Quarterly Report, during the three months ended 31 March 2023 and 2022, the company sold USD .7bn and USD .5bn, respectively, in principal balances of finance receivables under the MPSA and had USD 3.3bn of unused capacity as of 31 March 2023.

[2] It was reported in 2021 that Carvana “was under investigation by Texas regulators after selling vehicles some of its customers say they legally cannot drive.” In August 2021, it was reported that, the North Carolina Division of Motor Vehicles sued Carvana based on similar allegations and revoked Carvana’s dealer’s license in one county for violating dealer licensing laws, with the parties ultimately reaching a deal that resulted in a license suspension until January 2021. In January 2023, it was reported that Carvana admitted violating Illinois law by failing to timely issue license and registration documents and, to continue doing business in the state, forfeited a USD 250,000 bond and agreed to comply with various inspections by the Secretary of State Police.

[3] Specifically, they argued that the transaction, often referred to as an “uptier” transaction, should not be considered an open market purchase because, among other things, it was not open to all lenders. They argued that they were never offered the opportunity to exchange their holdings and were also never offered an opportunity to participate in the new superpriority USD 200m financing deal.

[4] In short, an ad hoc lender group objected to confirmation on two primary grounds. For one, SSB agreed to indemnify the PTL Lenders for their litigation costs and expenses incurred as a result of the uptier transaction, and then moved to assume the agreement as an executory contract. The lender group argued that the indemnity claims are based on the credit agreement, which is not an executory contract that can be assumed under the Bankruptcy Code, and that the indemnity claims should be disallowed or subordinated under sections 502(c)(1)(B) and 509(c) of the Bankruptcy Code. The lenders also argued that the plan failed to comply with the absolute priority rule by making a distribution of over USD 1.5m on account of intermediate equity interests.

A service of

Start your trial. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in