Braskem-Idesa 2Q23 Credit Report – It’s all down to the WC

Braskem-Idesa (BAKIDE) hasn’t set formal EBITDA guidance for FY23, and even less so for FY24. However, pressured by investor questions during the 2Q23 earnings call, management provided some rough numbers for the potential EBITDA this year and next, as well as for capex in 2024 (for 2023 there is actual guidance for the investments). Amid concerns about the company’s liquidity shown by some of the participants, executives even gave an outlook on the potential cash balance for the end of 2023 and 2024.

Therefore, with a very predictable annual debt service, no tax payments made currently, and an absence of shareholder distributions in the foreseeable future, in the end, it’s all down to the evolution of the working capital (WC) for the company to meet its liquidity outlook for this year and next.

BAKIDE reported an EBITDA of USD 40m in 2Q23, much better than the USD 26m of 1Q23 or the USD -33m of 4Q22, but still below the USD 96m posted in 2Q22, and even farther from the levels achieved prior to that. Management expects 2H23 to at least repeat the 1H23 performance, with a potential FY23 EBITDA of USD 120m-USD 150m. Meanwhile, FY24 could see an increase, with the EBITDA ranging from USD 150m-USD 200m. For our estimates, we’re going to take the middle points, at USD 135m for this year and USD 175m for the next.

As for the capex, BAKIDE has made a very important decision, postponing the first turnaround (major maintenance) of the polyethylene (PE) plant to 2025 from 2024 (to preserve liquidity, it had already postponed it previously for a full year from late 2023 to late 2024). This, along with some additional measures, is slated to slash the USD 63m budgeted operational capex for FY23 by up to 20%. Therefore, as the company already disbursed USD 34m for operational capex in 1H23, there would be USD 16m pending for 2H23. Meanwhile, USD 14m in strategic capex is left for the second half of the year (counting on a successful closing of the project financing for the new ethane import terminal by the end of 3Q23, as planned by the company). As for 2024, the total capex (strategic and operational) has been guided at USD 50m.

With all that, management indicated during the call that the cash balance could fall to USD 220m-USD 250m by year-end (down from USD 307m as of June). Here, again, we’re going to take the middle point, at USD 235m.

BAKIDE needs a minimum cash balance of USD 200m (including a USD 81m debt service reserve account, or DSRA) to operate normally. Therefore, we are calculating how the WC should evolve in the coming quarters for the cash balance to finish the year at the guided level, as well as stay above the minimum threshold at any time during 2024.

As Table 1 shows, BAKIDE can afford WC of USD -15m for each of 3Q23 and 4Q23 and still finish the year with the guided liquidity. In 2024, however, it would need to post a positive contribution of the WC to the free cash flow (FCF) of at least USD 22m to avoid falling below the USD 200m threshold.

Historically, estimating BAKIDE’s WC hasn’t been an easy task, as the contribution of the accounts receivable and accounts payable (also partially affected by the level of prices), on one hand, and inventory (production and sales volumes not always match), on the other, has been very volatile. However, we believe that those minimum required contributions of the WC included in our estimates are feasible. For instance, BAKIDE will no longer need to start building inventory up this year, thanks to the postponement of the turnaround to 2025 (the buildup needs to start a few quarters prior to the actual maintenance period).

Furthermore, the company still can make use of the existing WC facilities if needed (they’re in fact a true sale of accounts receivable, with no recourse to the company, thus removing them from the balance sheet). Obtained in 4Q22, they have a revolving nature during their two-year tenor. However, BAKIDE can only monetize the receivables at the pace it generates them, and as of June it only had some USD 25m on its balance sheet, thus somewhat limiting the size of additional deals (the initial transactions in 4Q22 amounted to a total of at least USD 89m).

The estimates, nevertheless, are also very dependent on the eventual performance of the EBITDA, which is highly affected by the PE and ethane (the main raw material) prices.

Higher production, sales offset PE spread tightening QoQ

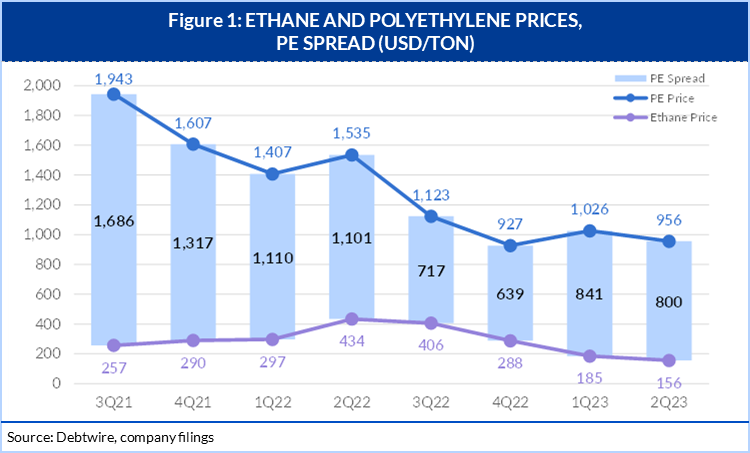

Despite a reduction in the price of ethane, the average PE spread for BAKIDE compressed in 2Q23 to USD 800 per ton from USD 841/ton in 1Q23 due to a greater reduction in the price of PE quarter-over-quarter (QoQ). In any case, while still far from the high levels seen until mid-2022, the spread has significantly improved from 3Q22 and 4Q22 (See Figure 1).

During 2Q23, BAKIDE produced 224.6 thousand tons of PE, 20.8% up from 185.6 thousand tons the previous quarter, with the utilization rate increasing to 86% from 72% over the same period (management expects to maintain the 2Q23 level during the rest of the year). Meanwhile, PE sales stood at 211.2 thousand tons (there was some inventory buildup), increasing 8.3% QoQ from 195.1 thousand tons. The higher selling volume helped dilute the fixed costs, with the operating income margin improving to -3.3% in 2Q23 from -10.5% in 1Q23.

Looking ahead, management indicated that PE prices have been trading above USD 900/ton in August in the US (USD 1,000-plus in Asia and Europe) and that a slight increase is expected for 2H23 when compared to 1H23, with a stronger recovery in 2024.

As for the costs, ethane price is now under USD 200/ton, after spiking in July due to some maintenance works in the US, but it usually increases toward the end of the year with the Northern Hemisphere’s winter, they noted. Meanwhile, an accident at a marine platform reduced Pemex’s ethane supply by 10,000-15,000 barrels per day (bpd) during two weeks in July (the Pemex supply, which is the cheapest for BAKIDE, averaged 36,000 bpd in 2Q23).

With all that, an average EBITDA in each of 3Q23 and 4Q23 of USD 35m is feasible, which would be somewhere in between the levels recorded in 1Q23 and 2Q23.

New waiver extension will be needed

BAKIDE announced in early July a nine-month extension (originally it was for six months through the end of June) of a waiver from its creditor banks in relation to a breach of a net leverage ratio covenant. Therefore, the company won’t be forced to comply with the maintenance covenant, which limits the net debt-to-EBITDA ratio to 5.95x, until the end of 2Q24.

Still penalized by the negative EBITDA of 4Q22, it finished 2Q23 with a net leverage ratio above 40x. While the substitution of past poor EBITDA figures with somewhat improved numbers will help to gradually reduce the leverage ratio in the coming quarters (gross debt isn’t expected to change in the immediate future), we are forecasting that it will still widely exceed the covenant limit in March 2024, standing at around 12.5x (See again Table 1).

Therefore, BAKIDE will need to negotiate yet another extension in early 2024, and in that case most likely for at least 12 additional months (we’re estimating leverage still at 11.2x by the end of next year).

A service of

Start your trial. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in