Beyond Meat: More revenue guidance cuts and cash burn – 2Q23 Credit Report

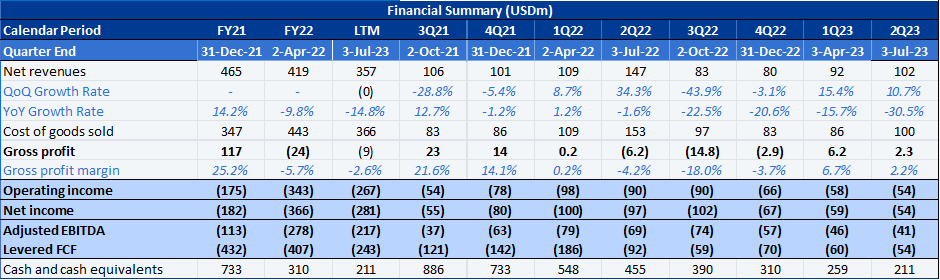

Beyond Meat (BYND) reported its 2Q23 earnings, which showed familiar themes: a 30% year-over-year (YoY) drop in revenue, a negative adjusted EBITDA of USD 41m, and a continuous decline in consumer demand in the steeply competitive market. BYND also once again cut its full-year 2023 (FY23) guidance to USD 360m-USD 380m, down from USD 375m-USD 415m in its previous quarter.

The company said that it plans to turn things around by distributing new products, marketing the health benefits of its products more heavily, and reducing prices. However, given its poor track record of meeting targets, BYND is seen as being prone to high execution risks. Confidence is extremely low that BYND will be able to achieve its goals, and there is also high uncertainty that its initiatives will materially improve the company’s performance and shift it away from its current trajectory towards more trouble.

BYND has failed to tame its high cash burn, and management has confirmed that it will not achieve its positive cash flow target in 2H23. According to our projections, we estimate that BYND will run out of liquidity by the end of 2Q24.

Competition & Valuation

In our Comps table, the peer average NTM revenue multiples for large-cap and small-cap companies are 2.3x and 1.1x, respectively, compared to BYND’s higher multiple of 5.0x. BYND’s net leverage of 2.7x is also materially higher than the net leverage of its large-cap and small-cap companies peers (0.5x and 0.3x, respectively). We believe there is a strong downside opportunity for the company as we see it trade away from its current high multiple and towards its peers, especially Oatly, which trades at 1.2x EV/NTME.

Our waterfall valuation uses our base estimate for NTME revenue of USD 343m and EV/sales multiples of 0.1x-2.0x. We found the convertible debt has a recovery rate of 24%, 30% and 36% at the low, base and high case scenarios, respectively. Based on the same multiples, we found the equity valued at 0 compared to its current share price of 12.

Financial Performance

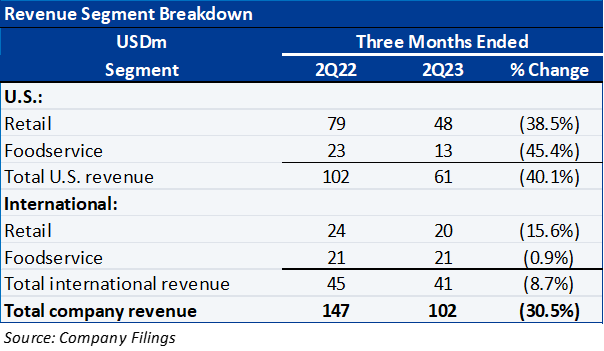

The company reported 2Q23 revenues of USD 102m, a 30.5% decrease YoY compared to USD 147m last year. The decline was driven by a 23.9% decrease in total pounds sold and an 8.6% decrease in net revenue per pound. All markets and channels were negatively impacted by weaker-than-expected demand for BYND category products, in particular the US retail market, which is its largest revenue stream. US retail channel net revenues decreased 38.5% YoY due to a 34.3% decrease in the volume of products sold, primarily reflecting weak category demand and the cycling of significant sell-in of Beyond Meat Jerky in the year-ago period. The 6.3% decrease in net revenue per pound was caused by higher trade discounts and changes in product sales mix, partially offset by increased pricing for certain items resulting from reduced sales to liquidation channels.

Overall US total net revenue fell by 40.1% YoY in 2Q23 to USD 61m, while total international net revenue fell by 8.7% YoY to USD 41m. The US foodservice channel experienced the largest decline, of 45.4%, primarily driven by sales to a large Quick Service Restaurant (QSR) that were not repeated and overall softer demand.

Gross profit was USD 2.3m, a 2.2% margin, from USD negative 6.2m, a negative 4.2% margin, last year. The improvement was impacted by lower materials costs, lower inventory reserves and lower logistics costs per pound. Gross profit and gross margin were partly improved because of a change in the Company’s accounting estimate associated with the estimated useful lives of its large manufacturing equipment made in 1Q23, which reduced COGS depreciation expense by approximately USD 5.1m, or 5.0 bps of gross margin, relative to depreciation expense utilizing the Company’s previous estimated useful lives.

BYND incurred a total operating loss of USD 53.8m, 55.2% margin, this quarter compared to a loss of USD 89.7m, 56.8%, in 2Q22, due to lower expenses from G&A, headcount, marketing and production trials. Total operating expenses decreased by 32% YoY and 12% sequentially to USD 56m. Adjusted EBITDA was negative USD 40.8m, or negative 40% margin in 2Q23 compared to an adjusted EBITDA loss of USD 68.8m, or negative 46.8% margin, in the year-ago period.

As for FY23, the company projects a net revenue range of USD 360m-USD 370m, a 14%-19% decrease YoY. Management also provided the following forecasts for the year:

- Gross margin, including the positive impact of the Company’s change in accounting estimates for the useful lives of its large manufacturing equipment implemented in the first quarter of 2023, is expected to be in the mid to high single-digit range.

- Operating expenses are expected to be USD 245m or less.

- Capital expenditures are expected to range from USD 20m to USD 25m.

Business Overview

Beyond Meat is a plant-based meat provider founded in 2009 in El Segundo, California. The company produces meat substitutes directly from plants, an innovation that enables consumers to experience the taste and texture of meat while enjoying the nutritional benefits of eating plant-based products. The company’s distribution channels are split into two categories: Retail and Restaurant/Foodservice. Flagship products include The Beyond Burger, Beyond Sausage, Beyond Chicken Strips and Beyond Beef Crumbles. As of July 2023, BYND products were available at about 190,000 retail and foodservice outlets in over 75 countries worldwide.

A service of

Start your trial. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in