CASE PROFILE: Bed Bath & Beyond enters Chapter 11 aiming to liquidate all stores

Bed Bath & Beyond Inc. (BBBY) filed its highly-anticipated Chapter 11 cases in the wee hours of Sunday, 23 April, stating it intends to completely liquidate its nearly 500 remaining brick-and-mortar stores after years of struggling to stay afloat.

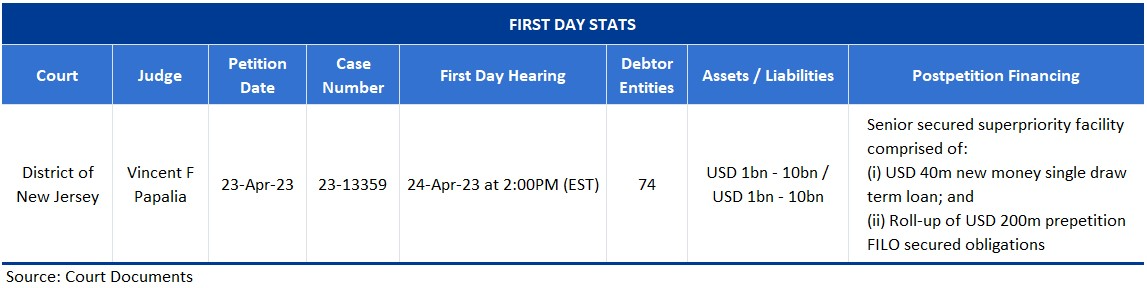

According to the first-day declaration of chief restructuring officer Holly Etlin, of AlixPartners, the company aims to liquidate all its stores and wind down. It comes to Chapter 11 armed with USD 240m in debtor-in-possession (DIP) financing, USD 40m of it new money.

Judge Vincent Papalia of the US Bankruptcy Court for the District of New Jersey scheduled a first day hearing for 24 April.

Debtwire Dockets: Bed Bath & Beyond Inc.

The company

BBBY was founded in 1971 as a small chain of specialty linen and bath shops called Bed ‘n Bath in the northeastern US, according to the first-day declaration. The two first stores launched in Springfield, New Jersey and Cedarhurst, New York, with each location corresponding to the area where one of the two founders lived at the time. By 1985, the company had expanded to 11 stores in New York, New Jersey, Connecticut, and California. The first Bed ‘n Bath “superstore” opened in 1985, a 20,000-square-foot outlet with a wide range of options intended to beat the more specific offerings of department stores at the time. In 1987, it took on the name it bears to this day, Bed Bath & Beyond.

BBBY went public in June 1992, trading under the BBBY ticker, and the stock surged over 100% in the following year. By 1999, Etlin says, the company’s sales passed USD 1bn, its eighth consecutive year of record earnings at the time. Entering the 2000s, it operated more than 250 stores and expanded into numerous states. By 2001, sales hit USD 2bn and it had more than 300 locations.

The declaration says that BBBY’s sales philosophy depended on getting customers into physical stores, where they found floor-to-ceiling merchandise and sales that would draw them to additional purchases. Etlin acknowledges the company was slow to adopt e-commerce when online sales grew exponentially, a decision that played a part in its ultimate decline.

Today, the company has 360 stores in the US and Etlin calls it a “preferred destination” in the home goods sale space. Its offerings comprise linens, foot prep, organizational products, and more. It also has a baby-oriented brand called buybuy BABY that markets products for infants such as nursery furnishings and baby essentials.

The debt

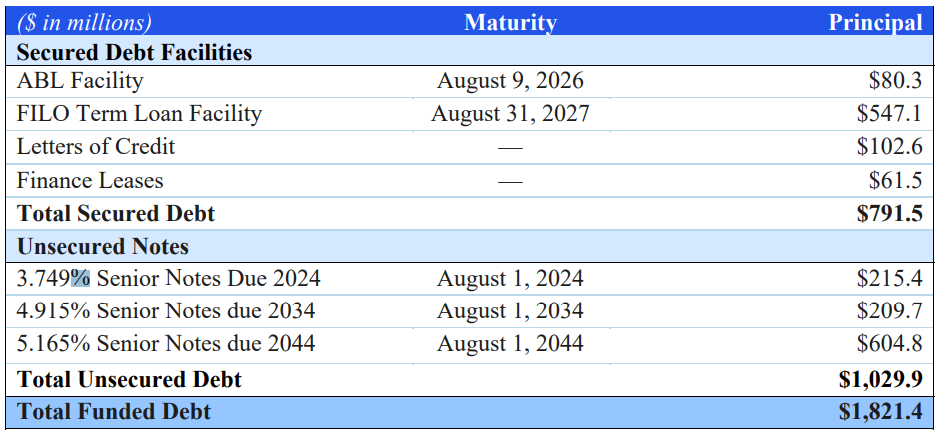

BBBY enters Chapter 11 with USD 791.5m in secured debt and USD 1.03bn in unsecured debt, for a total load of roughly USD 1.821bn. JPMorgan Chase acts as collateral agent on the ABL, due 2026, with Sixth Street Specialty Lending on the first-in-last-out (FILO) loan, due 2027. The ABL was originally in the amount of USD 1.13bn, later reduced to USD 300m.

Source: Etlin declaration

Signs of struggle

BBBY’s stock peaked at USD 80 per share in 2014, and the intervening volatility dragged that price lower since. By 2018, it traded at USD 14, which Etlin says amounted to the erasure of USD 15bn in value. All the while, its costs increased and margins shrunk from 16.5% in 2011 to under 4% in 2018. By early 2019, Etlin says, the company reported its seventh consecutive quarter of declining same-store sales, its first annual loss, and its first sales decline in the nearly 30 years since its IPO. The declaration also notes aging supply chain systems as a dragging factor on the business.

In March 2019, a group of investors voiced their frustration, Etlin says, leading to a board shakeup headlined by the departure of former CEO Steven Temares after 16 years. His replacement, Mark Tritton, attempted to institute a strategy he used in his time at Target Corporation by trying to enhance margins with a digital-first, customer-focused approach that also deployed private label brands. BBBY’s aging supply chain system ultimately collapsed under the stress of the overhaul, and it failed. Battered by those difficulties, the COVID-19 pandemic drove BBB further into the depths.

In late 2020, the company began to aggressively buy back stock to a total tune of USD 675m, later increased to USD 825m in December 2020 then again to USD 1bn in April 2021. Vendors worried that the company would run itself out of cash, and some reduced their business with BBBY, according to court documents.

The meme, the activist and the slide

In winter 2021, Etlin continues, BBBY became a “meme stock” promoted on social media sides such as Reddit — a wave that similarly caught hold of flagging companies such as GameStop – and it entered a “wild ride.” RC Ventures LLC invested in March 2022, taking a 9.8% stake and hoping to turn the company into another GameStop or AMC by parlaying the meme stock pump into financial benefit. RC began pushing for strategy changes, including selling off buybuy BABY or even the entire company and curtailing traditional marketing tactics. Etlin says that some decisions made at that point like ceasing mailed coupons harmed BBBY’s ability to sell in-store. It also implemented ill-fated distribution changes that rendered it unable to meet 2021 holiday demand, hurting sales and leading to roughly USD 100m in sales going unfulfilled. By the end of that year, net losses hit USD 559.6m.

After successive quarters of decline, Tritton was dismissed in June 2022 and filed a complaint against the company in New York State Supreme Court earlier this month alleging the company ceased making payments owed to him on a USD 6.75m severance agreement. Board member Sue Gove took over, hoping to put yet another transformation plan in place. Under her leadership, the company reduced its workforce heavily, and undertook inventory improvement initiatives. It also closed certain unprofitable or marginally profitable stores, and undertook an exit of the Canadian market – BBBY Canada is now conducting a wind-down under Canada’s Companies’ Creditors Arrangement Act (CCAA). Amid the transformation, RC took advantage of a stock rally and exited the company, selling off 11.8% of BBBY’s stock off. In the wake of that selloff, the shares dropped 20% after the announcement and another 35% after-hours when financial disclosures confirmed the exit. BBBY and former CFO Gustavo Arnal were also named in a USD 1.2bn shareholder class action securities fraud lawsuit that accused them of misrepresenting the company’s profitability and making false statements.

Further restructuring efforts

Throughout 2022, BBBY exhaustively pursued alternative proposals that would give it the runway to allow its transformation plans to play out, Etlin says. In August 2022, it secured USD 300m in new financing including an expanded USD 1.13 ABL facility and entering into the FILO term loan, originally worth up to USD 375m, with Sixth Street.

In October 2022, the company raised multiple exchange offers for its 2024 notes, 2034 notes, and 2044 notes. BBBY terminated the program after failing to satisfy certain conditions, even amid several extensions to the participation deadline. It also entered into an open market sale agreement for 12,000,000 shares with Jeffries, raising USD 115m. The 2022 holiday season brought further issues, with major inventory problems leading to multiple events of default under multiple financing facilities. Ultimately, it found itself in a USD 200m overadvance of its ABL. It entered a cash dominion period in January 2023. At that point, rumors of bankruptcy began to swirl, but BBBY averted them for the time being by announcing a public offering. With sales still dropping, income from the offering covered losses rather than replenished inventory, and the downward spiral continued unarrested. Other measures taken included a sales agreement with B Riley as agent offering up to USD 300m in common stock, and it entered into a separate stock purchase agreement with B Riley Principal Capital II LLC, the proceeds of which prepaid outstanding revolving loan obligations under the ABL. In the end, none of the measures could keep the company out of Chapter 11.

Bankruptcy and beyond

BBBY aims to fund its cases with the DIP financing from FILO lender Sixth Street. Of the USD 240m, 40m is new money and the rest would roll up prepetition debt. During the course of its bankruptcy, the company aims to close and wind down all of its remaining 475 brick-and-mortar stores, liquidating the company completely. Etlin’s declaration says that BBBY projects USD 718m in income from its closing sales.

As mentioned prior, BBB Canada Ltd and Bed Bath & Beyond Canada LP have already filed for CCAA protections in that country. They recently received an initial order from the Ontario Superior Court of Justice in that proceeding. Concurrently with the US filing, the debtors will seek a “cross border insolvency protocol” allowing coordination with the Canadian cases. As of the petition date, BBB Canada has nearly liquidated all its assets, and should finish by 30 April, Etlin writes.

The advisors

A service of

Start your trial. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in