Avianca 2Q23 Credit Report – Change in guidance, but showing improved results

Self-inflicted concentration problem for the regulator

Avianca has desisted from trying to acquire Viva, which until a few months ago was the country’s second largest carrier (tied with LATAM). The Colombian regulator took too long to decide, Viva’s financial situation deteriorated, in March it stopped flying… and the rest is history. In addition, Ultra, an airline owned by Viva founder William Shaw, stopped flying during April.

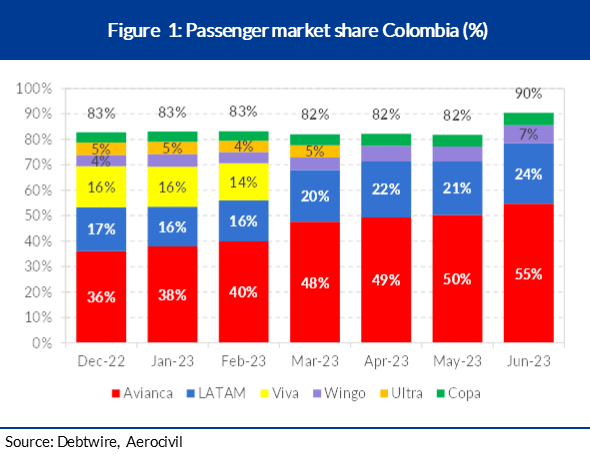

What was the end of this story? Higher concentration in the market, which of course is very good for the surviving companies. Avianca went from 36% market share in December to 55% in June, LATAM from 17% to 24%, and Wingo from 4% to 7% in the same period. That is, the 82%-83% market share that until February was held by six carriers, is now almost held by just two (Avianca and LATAM) that together have 79% of the market share (See Figure 1).

No more USD 3.4 cents for CASK ex-fuel

During the airline’s 2Q23 conference call, management ended the dream of a CASK ex-fuel target of USD 0.034 cents by year end, and replaced it with a range of USD 0.037-USD 0.038, citing higher inflation pressures. Avianca also said that because these pressures affect the entire industry, that it won’t lose its competitive advantage versus rivals. Given the appreciation of the BRL in the last couple of months, we saw a modest deterioration in the CASK ex-fuel for Azul and Gol, and the same is the case for Volaris (who operates mainly in Mexico, and saw the MXN appreciate versus the USD).

The exception is Avianca, which has been able to improve CASK ex-fuel, although it was flat relative to 1Q23. That is, densification efforts and other recent measures were only good enough to compensate for the deterioration in other areas. Now with the new CASK ex-fuel, clearly the progress in the coming quarters is going to be slower. If Avianca can profit from its increasing dominance in the Colombian market and raise prices, there shouldn’t be many problems (See Figure 2).

Financial highlights for 2Q23: Improving

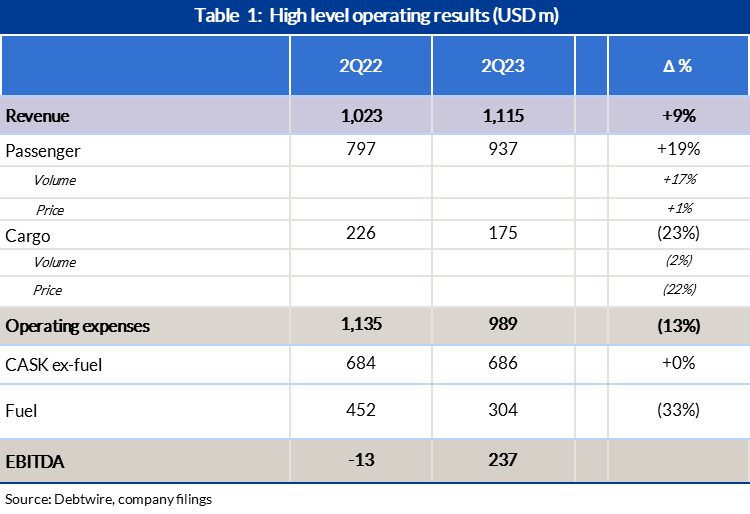

Numbers seem to be going in the right direction for Avianca. Revenues went up 9% YoY, above inflation, while CASK ex-fuel (in nominal terms) was flat in the same period. As a result, EBITDA was USD 237m, up from USD -13m in 2Q22. On the revenue side, if we separate passenger from cargo, we see an even better performance from the passenger segment. The 9% increase can be broken out between +19% for passenger and -23% for cargo. For cargo, the issue has clearly been shipping rates that must have declined significantly, as the total amount of cargo was down only 2% compared to 2Q22. The +19% increase in revenue in was mostly explained by a 17% increase in the number of passengers (See Table 1).

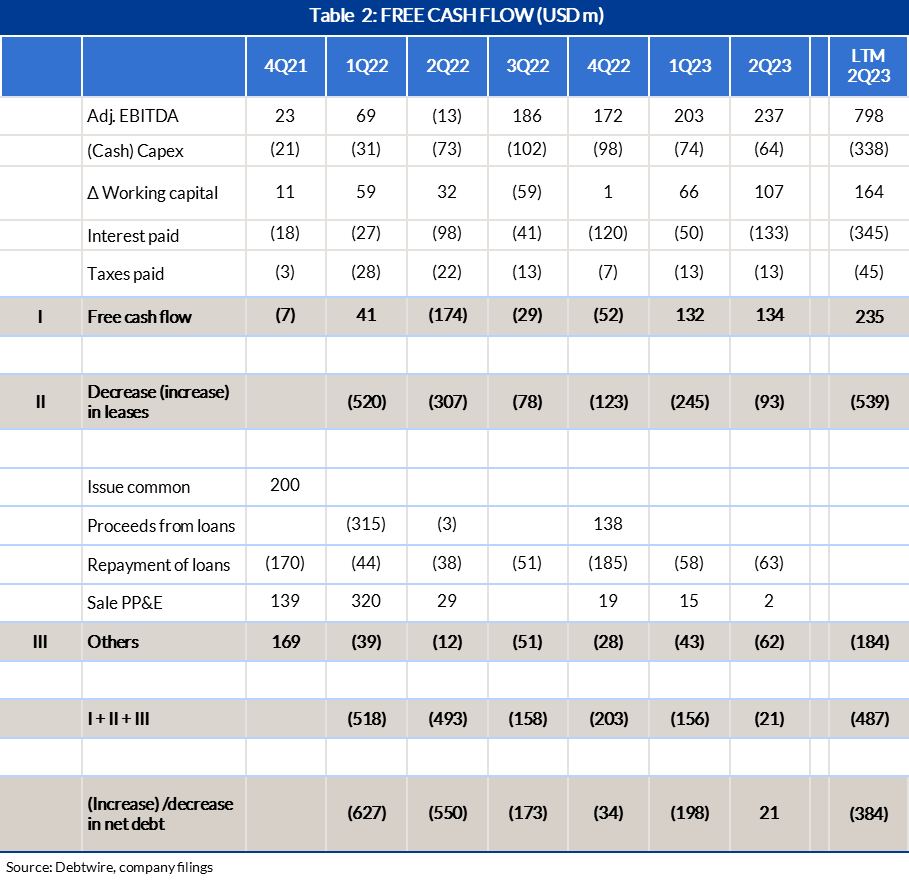

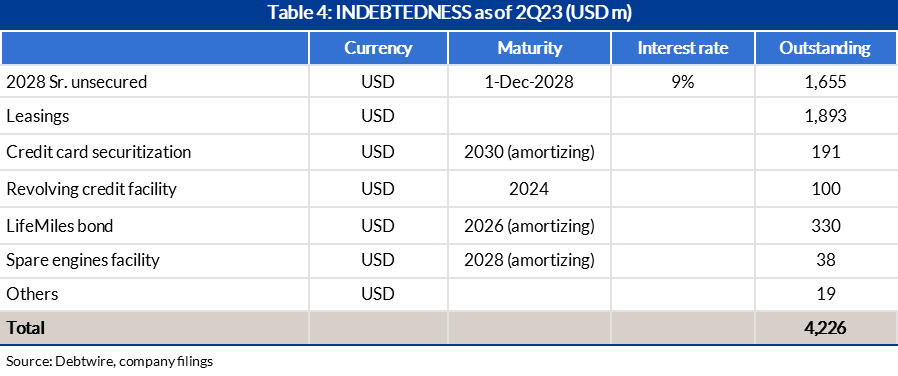

We calculated free cash flow to be USD 134m, on improved working capital (especially the air traffic liability line which is miles) and the higher EBITDA. As Avianca continues to increase its leasing portfolio (and probably will even more, if it picks up any planes from Viva), it added USD 93m in leasings (See Table 2).

KPIs follow-up

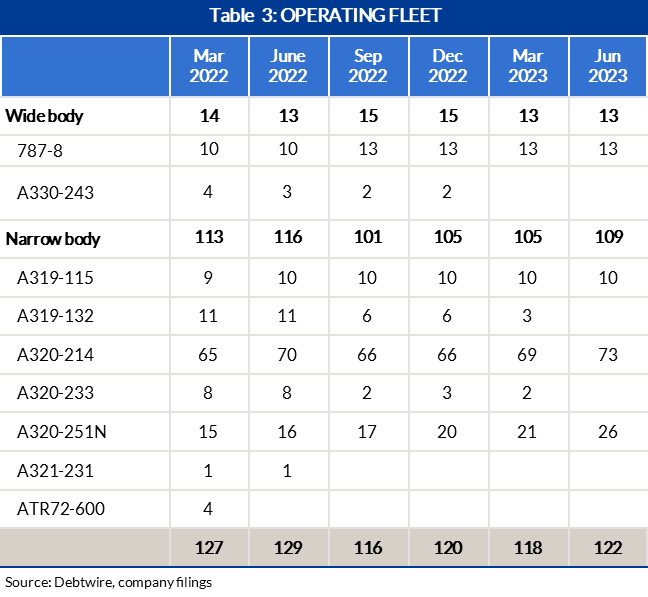

Avianca’s goal was to get to a CASK ex-fuel USD 0.034 cents, which now will be USD 0.037-USD 0.038. For that, Avianca needed to use its planes for more hours per day, which it is doing, getting to approximately 11 hours and 20 minutes in June (11 hours for 2Q23, on average) (See Figure 3). Additionally, it was going to have a more simplified fleet, in terms of the different types of planes it was going to have, and that number reached 4 in June when the last A319-132 left the fleet (See Table 3).

A service of

Start your trial. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in