Amyris’s liquidity still a concern despite recent cash inflow – 4Q22 Credit Report

By Glen D’Abreo and Sagar Joshi

Overview

Amyris Inc (AMRS), headquartered in Emeryville, CA, is a synthetic biotechnology and renewable chemicals company involved in the development and production of beauty, personal care and health and wellness products. It also offers sustainable ingredients used in the production of flavors & fragrances, food and beverages.

AMRS reports revenue from Renewable Products (chemicals used in beauty products); (87% of 4Q22 revenue and 82% of FY22 revenue); License fees and royalties (9% and 12%); and Collaboration and grants (4% and 6%). Product sales accounted for 66% of the company’s revenue in FY22, while services accounted for 34%.

Geographically, AMRS derives revenue from North America (73% of FY22 revenue), Europe (16%), Asia (7%), South America (2%) and other locations (1%).

Delayed Givaudan (GIVN) strategic transaction and term bridge loan

AMRS expected to close the strategic transaction in 4Q22 for an upfront cash consideration of USD 350m. However, the transaction was delayed due to antitrust requirements.

Following which, on 10 March, the company borrowed a USD 50m term bridge loan from which it drew USD 15m (on 13 March) for working capital requirements and general corporate purposes.

On 3 April, AMRS closed the agreement with Givaudan (GIVN), Swiss beauty and wellness products enterprise), to sell, assign or license some of its cosmetic ingredients.

The company received upfront cash consideration of USD 200m is expected to earn three-year performance-based earnout of USD 150m. Also, AMRS has entered into a long-term production agreement with GIVN to manufacture cosmetic ingredients for USD 150m.

Net debt

Pro forma net debt increased to USD 859m as of 15 April versus USD 257m at 4Q21 due to higher borrowings and reduction in cash to USD 79m on 13 March (4Q21: USD 483m).

Aprinnova JV acquisition

On 3 April, the company increased its stake to 99% in Aprinnova as it purchased 39 shares from Nikko and 10 shares from Nissa constituting 49% shares of the JV for a total consideration of USD 49m.

Liquidity

As of 15 April, the company’s liquidity stood at USD 9m. Considering the company’s cash burn, we estimate the company will need external financing as early as 2Q23.

Financial performance

Revenue increased 17% YoY to USD 76m in 4Q22, backed by growth in Renewable Products, partially offset by weakness in Licenses and Royalties.

In FY22, revenue fell 21% YoY to USD 270m due to the absence of large licence transaction. Excluding the impact of the DSM license transaction, revenue increased 36% YoY in FY22 due to rise in revenues from renewable products.

Renewable Products revenue increased 38% YoY to USD 66m in 4Q22 and 49% YoY to USD 222m in FY22 due to growth in in sales of consumer products, partially offset by a reduction in sales of ingredients.

License and Royalty revenue fell 50% YoY to USD 7m in 4Q22 and 81% YoY USD 32m in FY22. This was due to a higher base in FY21, which included DSM and RebM license transactions. Collaboration and Grants revenue declined 15% YoY to USD 3m in 4Q22 and 18% YoY to USD 15m in FY22, affected by weakness in DSM business.

The company announced 1Q23 expected revenue of USD 56m lower compared to USD 58m in 1Q22.

Despite growth in revenue, adjusted EBITDA deteriorated to negative USD 157m in 4Q22 and negative USD 521m in FY22, affected by a rise in manufacturing input costs and freight and logistics expenses. Moreover, SG&A expenses increased 43% YoY and 1.9x YoY to USD 135m and USD 494m in 4Q22 and FY22, respectively, driven by a significant rise in costs relating to marketing, selling and employee compensation.

This extraordinary rise in expenses was a result of higher spending for inbound airfreight and for importing ingredients intermediate products in 9M22. It is important to note that the company’s headcount despite operating at negative EBITDA has increased around three-fold to 1,598 as of 4Q22 (FY21: 980, FY20: 595). As a result, R&D and SG&A expenses increased significantly over the last two years.

In 4Q22, cash burn increased to USD 169m (4Q21: USD 130m), given the deterioration of adjusted EBITDA, partially offset by lower capex of USD 4m compared to USD 24m in 4Q21 due to the completion of the Barra Bonita fermentation facility project in 4Q22.

Cash burn increased to USD 652m in FY22 from USD 178m in FY21, mainly due to further decline in adjusted EBITDA and a rise in capex to USD 106m (FY21: USD 46m) resulting from investment to fund the fermentation facility in Brazil.

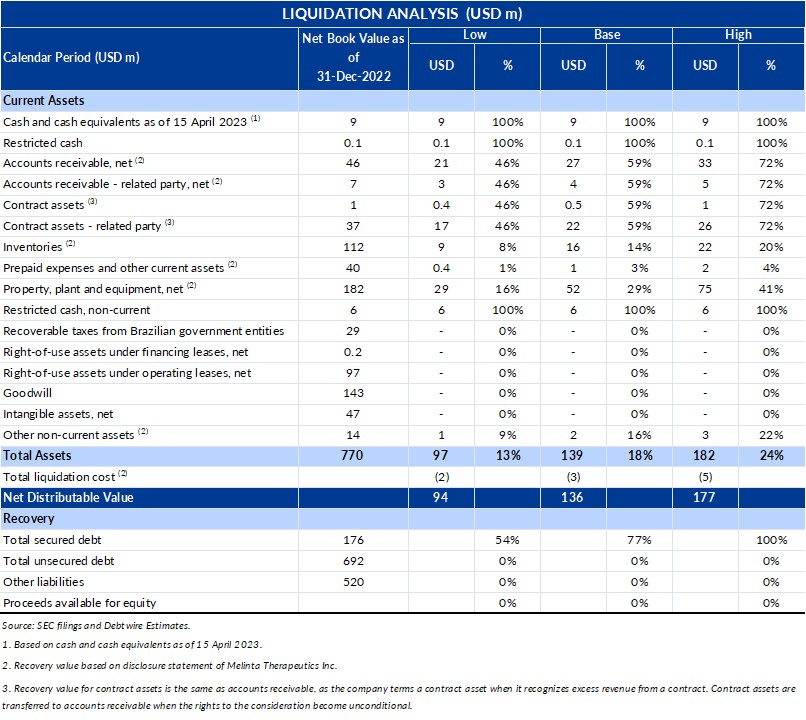

Valuation

In our liquidation analysis, the company’s secured debt gets 54% recovery in the low case, 77% recovery in base case and full recovery in high case. However, there is no recovery for the remaining debt holders and equity holders.

Considering the cash burn and dwindling liquidity position, the 1.5% convertible senior notes due 2026 last traded on 24 April at 23.3, down 49 points YoY, yielding 49.4%. While the stock price is down 78% YoY to USD 0.78/share on 27 April.

A service of

Start your trial. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in