Aegea levers up subsidiaries to upstream funds to holdco – 1Q26 Credit Report

As we mentioned in our previous report, Aegea decided to lever up its Corsan subsidiary to upstream dividends. Corsan’s net leverage stood at 1.6x, higher than the 1.4x we previously calculated, as that didn’t take into account the lower LTM EBITDA from the positive one-off effect of the PIS-CONFINS tax rebate the Rio Grande do Sul concession operator received during 1Q25 (Figure 1).

During 2024, Corsan paid BRL 463m in dividends and BRL 271m in interest. In 2025, those numbers were BRL 1.6bn and BRL 536m, respectively. In 1Q26 alone, the company distributed BRL 1.3bn in dividends and paid BRL 129m in interest. We calculate that the yearly interest expenses after the BRL 1.8bn domestic bond issuance in 4Q25 would exceed the previous annual amount of BRL 750m. It seems obvious to say, but the more debt Corsan has, the higher the interest expense bill and the lower the free cash flow it can generate to pay dividends.

Taking LTM EBITDA as reference, Corsan’s free cash flow was BRL 154m, meaning the company can absorb the incremental interest expense from the new debt, but further dividend payments will probably have to come from raising additional debt, unless it can significantly reduce capex (Table 1).

Given the ownership structure, Corsan’s dividends go almost entirely to the Parsan holding company, which must keep a portion to pay interest on its BRL 3.2bn debt, and upstream the rest to Aegea (75%) and the other shareholders (25%). We calculate that the interest cost is BRL ~540m per year, meaning that Corsan has to pay at least that amount in dividends for Parsan to be able to service its debt (amortizations start in 2029). Dividends to Aegea start above this figure.

In 1Q26, Corsan paid BRL 1.335bn, and Parsan received BRL 1.317bn and paid BRL 1.085bn. If we take 75% of this last amount, Aegea holding received approximately BRL 814m in dividends from Corsan (Aegea disclosed receiving a total of BRL 818m in dividends in the quarter).

Aguas do Rio (AdR)

For Aguas do Rio, comparisons with previous periods make no sense, as the subsidiary wrote off accounts receivable from several years ago in 2025 and restatements are occurring sequentially every quarter. Looking forward seems more useful.

Probably the two most relevant facts are that AdR got a 24.13% discount on the water it purchases, and that it was able to increase tariffs far above inflation. When Aegea received this concession, there were several elements that negatively affected AdR’s economic equation, like a smaller number of customers than initially anticipated and a more deteriorated condition of its infrastructure.

As with all concessions where the concessionaire more or less has some sort of guaranteed IRR, the ways to improve this IRR are (i) lower costs, (ii) higher revenue, (iii) lower capex, and (iv) longer tenor of the concession. After a years-long conversation, it was agreed that Aegea was going to be able to purchase water at a discount from CEDAE (a government entity). In addition, Aegea also was able to raise the tariff significantly above inflation (traditionally, tariffs rise in line with inflation and a relevant portion of a concessionaire’s profit comes from being operationally more efficient than a government company would be).

To provide some perspective, during 1Q26, Aguas do Rio spent BRL 388m to purchase water, down 28%, or BRL 162m, from BRL 540m in the same period last year. This item alone represents BRL ~650m annually in incremental EBITDA.

In terms of revenue, every 100bps increase above inflation, based on 2025 figures (which are over-penalized because of the restatements), represents BRL ~75m in incremental revenue and EBITDA. In 1Q26, AdR increased tariffs 9.75% for zone 1 and 8.09% for zone 4, both far above the 4.1% IPCA rate.

Considering both of these effects, we can think of BRL ~1bn in annual incremental EBITDA versus previous year, excluding the receivables write-offs.

During the quarter, Aegea only sent BRL 19m to AdR, but we suspect it won’t be only this amount. Free cash flow for the quarter was BRL –443m. Even with the higher revenue and lower costs, the interest bill keeps growing and it will take time for Aegea to stabilize it.

Holding company flows and amortizations

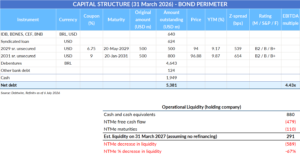

Management mentioned during the conference call that it doesn’t expect to need additional funds at the holding company level for the next 12 to 15 months (unless new M&A opportunities arise). At the end of March, Aegea had BRL 4.6bn in cash and BRL 610m in amortizations in the next 12 months. A big unknown is how much more in dividends it can collect, considering that a very large portion of the dividends collected in the last 12 months came from Corsan, and as we have mentioned, unless Corsan keeps levering up, the flow of dividends will diminish (Figure 2).

Also, Aegea fully hedged its USD-denominated funding, as it has 100% of its revenues in BRL. When the BRL appreciates, the derivates go south and Aegea needs to pay up.

During LTM 1Q26, the free cash flow at the holding company level was BRL -4.9bn. Out of that, BRL 2.2bn corresponds to the net financial expense on the derivatives Aegea had to pay that (unless the BRL further appreciates, it won’t have to pay this anymore). Dividends paid represented another BRL 1bn, and according to management’s words during the call, they would be “significantly reduced” (and we think even suspended, if needed). However, this alone won’t be enough (Table 2).

Management mentioned the “dual mandate” of having a minimum cash balance, absent of any new M&A, of BRL 1.5bn, while keeping net leverage below 4x. At BRL 4.6bn, the company still has cushions, which coincide with the fact that management mentioned it probably won’t need to take on new funding in the next 12 to 15 months.

A service of

Start your trial. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in