ECM Highlights 9M23: Green shoots of recovery

Powered by Dealogic data, ECM Highlights reviews ECM activity across Americas, EMEA and APAC in the last quarter and year-to-date. All data correct as of 1 October 2023.

Global ECM: Arm-azing grace, how sweet the sound

While Equity Capital Markets remain below where some might like them to be, big deals in the US and Europe have started to sow seeds of optimism that there are better times ahead.

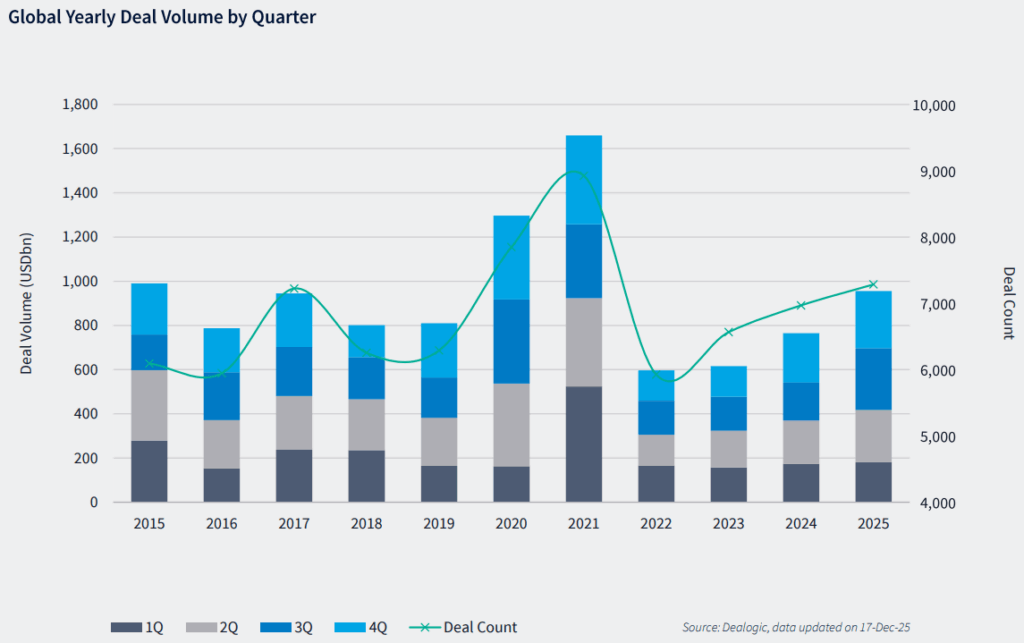

Issuance volumes of over USD 470bn so far in the first nine months of 2023 means global issuance sits 3% higher than at the same stage last year, with Americas exchange activity up 37% from this point in 2022. Volumes for EMEA and APAC have shrunk in 9M23 compared to 9M22 though, according to Dealogic data.

The USD 5.3bn IPO of Arm Holdings [NASDAQ:ARM] was the largest deal of 3Q and the largest US deal so far this year. While the stock has been volatile since pricing, the fact the long-awaited deal was done at all is still deemed a positive by many deal-starved ECM practitioners.

Substantial follow-on activity also boosted third-quarter volumes, including a USD 2.7bn block in AerCap Holdings [NYSE:AER] and a USD 2.5bn block trade in London Stock Exchange Group [LON:LSEG].

“There are encouraging signs of a continued reopening,” said Andre Briscoe, head of the EMEA ECM syndicate at Bank of America. “I don’t believe a couple of priced IPOs triggers a sudden flurry of IPOs in Europe. But hopefully, there are signs of continued reopening.

“It is gradual, but RFPs are now coming in and a pipeline is building.”

The USD 150bn worth of issuance in 3Q23 globally was slightly below the USD 152.3bn recorded over the same period in 2022, in part due to Porsche’s [ETR:911] mega deal in September 2022, but recent activity has been spurring the modest recovery in issuance over 9M23.

Volumes in the Americas grew 63% to USD 63.6bn in 3Q, above the USD 39bn seen in 3Q22.

Consistently higher volumes in the US are driving the uptick in global ECM issuance from the first 9M of 2022, but a drop in Middle Eastern IPO volume alongside a 23% fall in Asian ECM volume, ex-Japan, has weighed down the global ECM recovery year to date.

The US was the top global exchange for ECM activity in 3Q23, boosted substantially by the IPO of Arm, with volumes of just over USD 55bn. In 3Q22, the US was the second most active exchange in terms of ECM volume with USD 35bn of issuance, behind China which registered USD 53bn of volume; China had USD 29bn of issuance in 3Q23.

The US taking top spot means it has now ranked as the top global ECM exchange for four quarters in a row.

The LSEG block was a boon for the much-maligned UK stock exchange, the LSE itself. The sell-down in the exchange meant the UK ranked fifth in the Dealogic global exchange league table in 3Q up from seventh in 3Q22. Earlier sell-downs in LSEG this year allowed London to take third place in 2Q23.

Global IPO volume stood at around USD 33.2bn in 3Q, still well below the average for the benchmark asset class in global ECM, and down from USD 47bn in 3Q22.

Over USD 86bn of follow-on activity dominated ECM volumes in the quarter, down quarter-on-quarter, but the first nine months of the year are 12.5% higher than 9M22.

There was global convertible bond issuance of around USD 29.3bn in 3Q23, up from USD 21.3bn in 3Q22. Total global CB issuance in 9M23 is around 50% higher than in 9M22.

Should follow-on activity continue and more chunky IPO sellers, like Arm, decide to brave equity capital markets, there will be optimism that a recovery in equity capital markets could be around the corner.

Americas: ARM-ing up

ECM 3Q volumes for Americas hit USD 63.6bn from 433 deals, 63% up compared to the same period last year, but slightly below the USD 66.5bn volume achieved last quarter.

The pick-up in volumes in the US was the main driver of growth for the region. Arm's IPO followed by a couple of other listings has raised hopes of a US market reopening.

The deal came as 3Q recorded USD 9.3bn in deal volume across 44 IPOs on US bourses, marking an upward trajectory on both 2Q (USD 8bn) and 1Q (USD 3.1bn). The performance is better than the same quarter last year (USD 3.1bn from 37 deals) but is considerably lower than the heights recorded in 2021, when Q3 saw USD 51b across 190 deals, and 2020 and 2019 which also recorded higher deal volumes.

Recent weeks have also seen the IPOs of Klaviyo [NYSE:KVYO], and Instacart [NASDAQ:CART]. Despite their bubbly debuts, the longer-term aftermarket performance of the three big deals will indicate whether the window is really open, and if the wave of optimism will ripple across issuers and advisers alike.

“We are at a crossroads, as we entered bull market territory earlier this year. Both macro and the markets are moving in the direction for a reopening of the capital markets,” said Paul Abrahimzadeh, Citi's co-head of equity capital markets for North America.

“In the past few months, investors started to anticipate that the economic recession would be shallow and there would be a quick bounce back. Markets stabilised because people felt good about the outlook, inflation and rates,” he said.

ECM volumes in 3Q for the US reached USD 58.5bn across 362 deals, less than 2Q’s USD 61.6bn from 374 deals, but higher than 1Q’s USD 44.2bn. The quarter also had higher deal volume than USD 36bn seen in the same period last year.

In the coming weeks, all eyes will be on Birkenstock. The German footwear brand, which is owned by LVMH-backed private equity firm L Catterton, has set a price range between USD 44 and USD 49 per share for its listing. Amer Sports, the maker of Wilson tennis rackets and Salomon ski boots, has also filed confidentially for a US initial public offering that could value the group at as much as USD 10bn.

“The threat of “higher-for-longer” interest rates continues to temper the enthusiasm of the market and thus of potential issuers and their bankers, but there is more preparatory activity now than at any time in the last 18-24 months,” said Jeffrey Cohen, a Capital Markets Partner in Linklaters’ New York office.

Secondaries, meanwhile, recorded a quieter pace. 3Q23 reached USD 33.9bn across 275 deals, less than 2Q’s USD 39bn, but higher than 1Q’s USD 26.3bn. This figure was still higher than the deal volume seen from the same period in 2022. Equity-linked grossed deal volumes of USD 15.4bn across 43 deals, slightly up from 1Q and 2Q which stood slightly above USD 14.4bn.

“Half of the [secondary] offerings we have seen priced lower than they did on previous deals from the same seller, which signals an adjustment to a new valuation environment,” Abrahimzadeh noted.

There are still a few months to go before the end of the year, but even if 2023 does not end in a boom, there is a gradual return to a meeting of the minds between issuers and buysiders that could create a more favourable environment for issuance next year. A tug-of-war on valuations seems to have reached a stage of realignment, Abrahimzadeh noted, with projections becoming more rooted in sustainable objectives and track record.

“The market is much more rational,” he said.

EMEA: Giving ECM a Schott

EMEA is lagging the US, but steps toward a reopening have been largely welcomed by both issuers and buysiders. Valuation expectations have gradually realigned after significant clashes prompted the postponement of several deals in previous months.

Schott Pharma, the German medical vials and bottles maker, jumped 16% on its first day of trading after pricing in the upper half of its indicative range. Oman's OQ Gas Network, the pipeline business of the sultanate's state oil conglomerate OQ, attracted considerable international and local demand.

IPO volumes for Q3 were significantly up from Q2, at USD 6.5bn over the previous quarter’s USD 4.1bn, according to Dealogic, and better than Q1’s USD 5.6bn.

Both German gearbox maker Renk and French software firm Planisware are now (as of 2 October) in IPO bookbuild mode, which signals more activity down the line. There are other candidates in early to mid-stages prep that could accelerate launches to make the most of the improving sentiment.

The quarter also featured the EUR 605m listing of Thyssenkrupp’s [ETR: TKA] hydrogen division Thyssenkrupp Nucera [ETR:NCH2], the GBP 292m IPO of CAB Payments [LON:CABP], the huge IPOs of Romania’s Hidroelectrica [BUC:H2O] for the equivalent of USD 2bn, and USD 1.2bn listing of Saudi Arabia's Ades Holding, which is yet to start trading.

“In upcoming IPOs there is definitely more of a focus on established businesses with quality earnings and which are profitable. I would say that any company that has quality earnings will receive an audience in a public markets setting,” Bank of America’s Briscoe said.

While new listings are on the rise, EMEA ECM issuance at large still lags previous quarters. Volumes across deal types in Q3 stood at USD 27bn, down from the second quarter (USD 35.5bn) and the first quarter (USD 37.6bn). It is also down compared to the same quarter in 2022 (USD 29.8bn) and 2021 (USD 53bn).

A similar trend characterised follow-on issuance. A more muted series of months has been largely pinned to cautious issuers and stock prices remaining off desired performance levels. Equity-linked though paints a rosier picture. 3Q’s USD 3.3bn deal volume is higher than 2Q’s USD 2bn, but still down on the first quarter’s USD 5.4bn. Eni [BIT:ENI], the Italian energy and conglomerate, got strong uptake for a EUR 1bn convertible bond last month.

Davide Basile, a partner at Redwheel, argued that there was no summer recess for CB markets this year, with August issuance “standing at levels surpassed just three times during the last decade.” September kicked off in the same vein. “In the first week, CB markets have been presented with nine deals across a range of sectors, in just three trading days since the beginning of the month,” he said.

In September, Snam [BIT:SRG], an Italian gas distributor, raised EUR 500m in senior unsecured EU taxonomy-aligned transition bonds due 2028.

These might still be only a few silver linings, but it’s enough to give issuers confidence it is worth giving the markets a try.

APAC: Japan and India rise as China de-risking continues to pinch

Equity fundraising deals through Asian exchanges hit the lowest mark since the early days of the COVID pandemic in 3Q, though increasing activity from Japan and India helped make up for some of the grounds lost to China de-risking.

The region’s companies raised a combined USD 59.9bn from equity capital markets in the July-September quarter, 60% of USD 84bn recorded in the year-earlier quarter, or down roughly 5% from the second quarter, Dealogic data shows.

“The biggest challenge, if you look closer, is the valuations that companies are coming at,” said a hedge fund manager, adding that deal valuations at a time of high interest rates dictate investors’ risk appetite more so than company fundamentals.

Both the IPO and follow-on markets continued to soften in the just-ended quarter, while the equity-linked bond asset class was the dark horse.

IPO proceeds from the region totalled USD 17.4bn, just a little about half of the USD 32.6bn recorded in the same period a year earlier, or 30% below the second quarter’s USD 25.28bn.

China continued to top the region’s IPO market by pricing USD 11.7bn worth of new share listings, which was nonetheless down from USD 25.1bn in the same quarter of 2022.

India, backed by its growing population and prospects of gaining a bigger share in the global supply chain, rose to the region's second spot in the third quarter by raising USD 2.5bn from maiden share offerings, versus USD 450m in the same quarter last year.

Japan, supported by a string of favorable government policies to improve investor returns, raised USD 1.1bn in the third quarter, also a sharp rise from a year earlier when USD 265m was recorded.

Hong Kong closed the third quarter as the region’s number four by pricing USD 1bn, which was a far cry from USD 8bn a year ago.

With investors being demanding on valuations, issuers either postponed their IPO or had to swallow a lower price tag than planned, which increased the likelihood of a down-round, said a second investor.

In some cases, just one down-round may not be enough. “It has to be an attractive down-round,” the second investor said.

Take TUHU Car [HKG:9690]. The Chinese integrated online and offline platform for automotive services backed by Tencent [HKG:0700] raised USD 138m in September from a Hong Kong IPO that was priced at the cheap end of HKD 28 per share, which essentially valued the company 30% below its last private round, the two investors said. They still didn’t buy into the IPO while they acknowledged a 30% valuation cut is considered a sincere gesture by the company.

The IPO was eventually backed mostly by friends and family, with merely USD 3m allocated to hedge funds, the investors said.

That explained the fact that out of the 219 listings priced in the third quarter, only a handful managed to raise USD 500m or above.

TUHU has gained around 10% since its late-September debut, though its daily volume is thin.

The Hong Kong IPO market should improve slightly in the final quarter of 2023, according to the first investor.

Not only has the number of IPO filings increased, the city is finally seeing some market-size deals, including a potential USD 500m IPO of J&T Global Express, an Indonesia-based global logistics service provider. The deal’s pre-marketing will kick off in early October.

Equity-linked defies gravity

Asia’s convertible bonds market printed USD 10.4bn worth of notes in the third quarter – the third straight quarterly improvement. It was also the best quarterly showing since the USD 13.7bn recorded in the first quarter of 2021.

A string of reasonably priced deals from high-profile quality issuers with solid use of proceeds so far this year – a rare scene for the asset class – has helped the market sustain the momentum from quarter to quarter, a CB banker and a CB investor agreed.

Among the most well liked deals were JFE Holdings’ [TYO:5411] JPY 90bn (USD 613.8m) offer and LG Chem's [KRX:051910] USD 2bn dual-tranche exchangeable bond into LG Energy Solution.

It has become almost mandatory for bankers to engage investors prior to launch to make sure deals get covered.

The banker said he would remain cautious nonetheless as he doesn’t foresee a robust pipeline so long as investors remain wary of China.

The region’s follow-on market raised USD 32.1bn worth of placements or blocks, 26% below the USD 43bn seen a year earlier, though up from the second quarter’s USD 30.7bn.

Similar to the IPO market, other than China’s A-share transactions, India and Japan dominated a big chunk of the follow-on market in terms of USD volume and deal count.

A service of ![]()

Shape your future with Dealogic.

Explore unlimited content like this, available only in the platform.