Middle East conflict muddies issuance outlook after storming start – ECM Highlights 1Q26

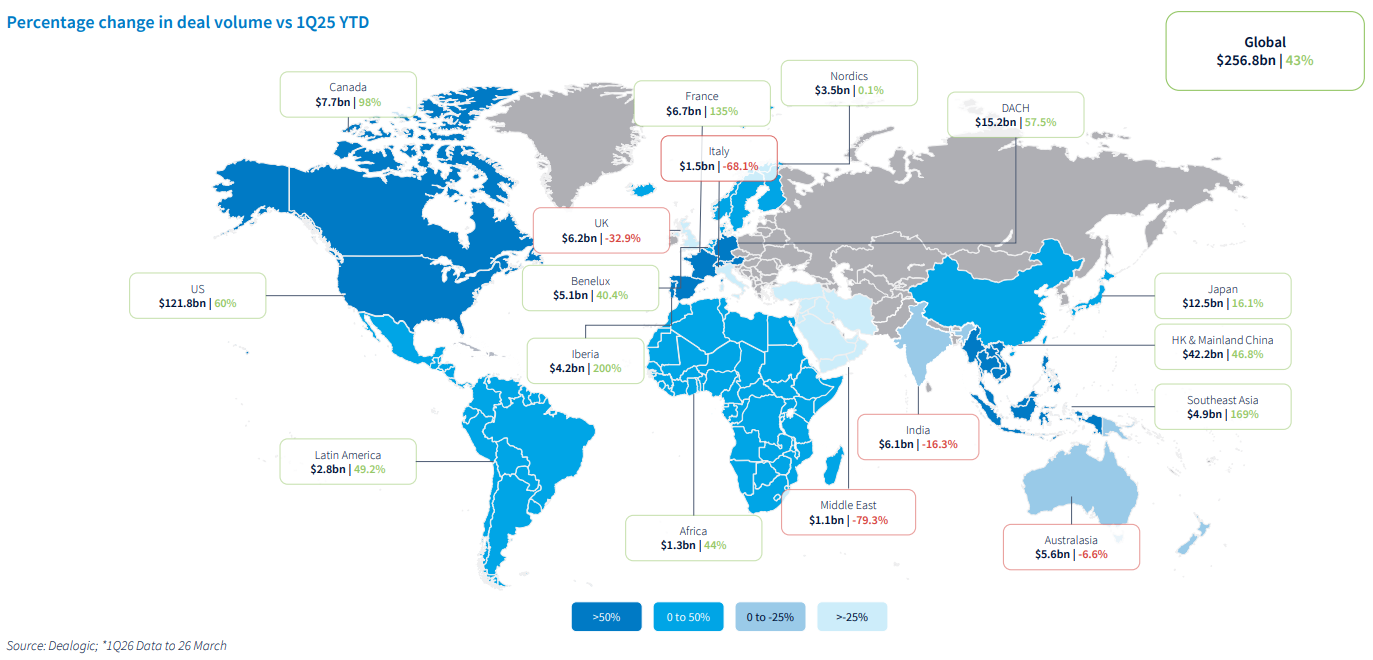

Global ECM volume soared 43% year-on-year (YoY) to USD 256.8bn in the quarter-to-date (26 March) but this epic haul could have been higher still if war in the Middle East had not intervened.

Joint US-Israeli strikes on Iran arrested momentum in March. In January-February, volume of USD 164.6bn had climbed 62% YoY. As March heads into its final trading sessions, the monthly tally is USD 90.8bn, up just 11% YoY.

The ongoing fallout of the Iran conflict obscures issuance visibility for the rest of the year.

ECM dealmakers are famously adaptable beasts, able to pivot their pipelines to focus on follow-ons and equity-linked deals when an environment of geopolitical turmoil and heightened macroeconomic pressure makes a strong IPO run fanciful.

This was indeed how they delivered volume growth in March, pushing benchmark block trades that leant into investors’ preference for larger transactions in proven names offering greater liquidity in times of stress.

Eight out of 10 of the largest ECM deals in March 2026 were follow-ons, including the huge EQT-led USD 6.3bn clean-up trade in Galderma; a USD 5bn primary offer from Zurich Financial backing its takeover of Beazley; and Blackstone, Carlyle and Hellman & Friedman undertaking a USD 3.5bn sell down in Medline.

Some notable oil and gas blocks also got away in the past month, as tanker captains dropped anchor in the Strait of Hormuz and oil prices soared.

A service of ![]()

Shape your future with Dealogic.

Explore unlimited content like this, available only in the platform.